A 25 year veteran of the supply chain and logistics industry blogs on all things logistics. Experience in 3PL, automotive and consumer goods logistics help bring a unique insight to this topic

A fantastic discussion over at Supply Chain Index on the measurable differences between a "Supply Chain" and "Value Chain" (Value Chain vs Supply Chain). Most use these terms interchangeably and this blog post really has given me cause for thinking about these terms. I even realized I did not have a tag or label for "Value Chain" which shows I thought of them as synonyms; Which they clearly are not.

Abby Mayer

Just as "logistics" has morphed into "supply chain" "supply chain" is now morphing into "value chain" in our industry lexicon. However this blog post makes us think this over.

I am starting to think we have to reemphasize that these three terms are three distinct elements of the overall "cash to cash" cycle and getting goods to market.

It was a fantastic conference and I really enjoyed running track 6 - Energy and Infrastructure. We had great presentations from Walter Zimmermann, the Kansas City Southern Rail, the Environmental Defense Fund, The Port of Long Beach, Smartway (EPA Partnership with Industry) along with case studies on natural gas implementations which occurred at two major shippers. These successful implementations are truly the "win-win-win" where the companies have lowered costs, done great things for the environment and have contributed to our nation's move to a domestic fuel source.

Two highlights of the conference were to hear T. Boone Pickens speak (Read about the Pickens Plan here) and I actually was able to attend a luncheon with him. What a fantastic person and his work to get this country an affordable domestic fuel source should be praised by everyone in the country.

I also was thrilled and excited to see Erik Wahl (The Art of Vision) motivate us about creativity and innovation in a very unique way - he paints incredible pictures during his talk! Below is a Youtube video of him (not the one at CSCMP) and you will immediately see what I mean.

I have been attending these conferences for years and this was the best one I have ever been too. The energy, excitement and pertinent topics were all fantastic. I am already looking forward to Denver 2013!

You have heard me say over and over again that the ultimate goal is not just cost reduction it is the actual elimination of costs. Think e-books and iTunes® and think of all the costs which just were totally eliminated. No one figured out how to "reduce" the costs of shipping books rather they just eliminated the shipment all together.

An early trend I am watching now is the idea of 3D printing. This may even be too early to call it a "Mega-trend" however I think it is something we should be aware of. Just like the elimination of shipments of things which have been digitized (books and music) the next frontier are physical "hard" parts.

At the end of this post is a neat little video which explains this technology. Think of it this way: If you need to make something which is made out of one material you could just load the material, load the digital specs and the printer does the rest. The key for Logistics people is the part is printed at the point of use and on demand. This has two implications.

First, as this gets better and better and costs come down for the machines more and more product will be made this way. This means less product is made at some far away factory and shipped. This will result in a continued headwind on shipping volumes.

Second, this will also dramatically reduce or even eliminate inventory. No need to stock 30 days supply of something when you can "print on demand". This also puts downward pressure on freight demands as less and less distribution will be needed (also has huge implications for warehousing).

To the left you can see what these machines look like. I just found these off the Tasman Machinery website (no endorsement just a good picture). Like all electronic machines during their infant stage there is a lot more development to happen and I am sure it will happen.

Here is a picture of actual wearable shoes made with 3D printers and above is a picture of a model / replica of a ship made with 3D printers.

You may look at these products and say there is nothing to worry about as it will take a long time for these types of products to be brought into production. Of course, I would have to remind you this is what people say about all disruptive and new technologies at the beginning.

I think this will develop rapidly and this could be the "new normal" for a lot of manufacturing of sub assemblies and parts. As I said above, this will eliminate the need to ship this product and, of course, lessen the demand for transportation. One can clearly imagine a day when you walk into a store, need a basic product and rather than the hassle of inventory and distribution, the store clerk will just "print on demand" for you in the store. Huge implications for freight costs and demand, inventory and warehousing and S&OP processes.

According to a blog post by Richard Gottlieb at Global Toy News we may be at a tipping point as it relates to the use of 3D printing in the toy industry. He rightfully highlights the implications and benefits of this technology by saying:

If you own enough 3D printers, why would you need to own any inventory? You could print out on demand. It’s JIT (Just in Time) in its truest sense.

If you can print out small batches without the need for molds or factories? Anyone can enter the marketplace with a new item. The only cost is for the material.

If the need for factories and engineers declines, what happens to people who currently hold those jobs?

Again, this is pre "mega trend" stage but watch it closely as these types of technologies have a way of taking off.

Below is a great little video explaining what this is all about:

Over at the Transplace blog they provide some analysis on the most recent Morgan Stanley release. The words which caught my eye were they now expect truckload capacity to be "readily available" for the remainder of the year.

This has been the trend for a few months with some artificial "greenshoots". While I have been predicting this for the better part of the summer I still believe the issue is companies are really reluctant to bring back inventory. They would much rather error on the side of "running out" than stocking too much and that means less freight is moving.

I will be starting a new feature this week called "Macroeconomic Monday®" where I will be reviewing the macroeconomic trends from the previous week and what is up coming. I will also add commentary as it relates to the logistics industry. Hopefully this will become a "must read" for you every Monday morning.

You can always search for it on my blog by going to the label "Macroeconomic Monday®" and look for it on twitter at #macmonday® (without the ®).

The Environmental Defense Fund really puts out good science. They are truly non partisan and report the facts as they are known. I just read this posting called "Getting Natural Gas Right" and I was both intrigued and encouraged. The conclusion is simple (and those who take ideological positions on science will not like it): If large amounts of methane are released into the atmosphere due to leakage, the use of Natural Gas will be worse, not better, than what we are doing today.

However, there is great news. If prudent measures are taken to ensure the proper drilling, transportation, storage and combustion then natural gas becomes a fantastic fuel to help us move to a low carbon future.

As my readers know I am hosting Track 6 (Click on Track 6 here and see the tracks objectives) at the Council of Supply Chain Management Professionals annual conference in Atlanta next week. This track will cover all aspects of Energy and Infrastructure issues facing both our industry and the globe. We have expert speakers from all facets of the discussion and I can assure you we will challenge the status quo thinking!

I am especially excited to announce to have Elena Craft on our panel. Elena Craft has had a stellar career as a health scientist for the Environmental Defense Fund (EDF) and I am proud to have her on our panel. I have linked to her biography above and I would also encourage you to read her great blog postings at The EDF News and Blogs Section. She will challenge us to think differently about what we are accomplishing.

Her presentation is on Monday afternoon, October 1, 2012 in Track 6 at 4:45.

I really am looking forward to CSCMP 2012 in Atlanta this year. I am hosting Track 6 - Energy and Infrastructure where we will have a very robust and exciting discussion on the role energy and infrastructure play in your supply chain - and it is a big role.

Energy costs can consume almost 40% of your total transportation cost structure and of course the Country's infrastructure can decide how efficiently you can get goods to market. We will cover everything from the macro economic outlook for energy to two great case studies on how to convert your fleet to natural gas and alternative fuels.

The exciting part of this is we will cover the spectrum. Do not expect to have 8 sessions where people all agree (I remember a saying "If everyone in the room thinks alike, someone is not thinking).

We start with a well known economist on the overall macro outlook for energy in the US: Walter Zimmermann (A very interesting short biography). He has been seen on CNBC and other national news shows and has a very interesting and data driven view on the potential for energy independence and what is happening in the energy markets today.

Following Walter we will have multiple presentations from Rail executives, scientists and practitioners on what is happening in the world of energy and infrastructure. It will be a very exciting and timely topic.

I look forward to seeing everyone at the conference and let's use this to really challenge our thinking, learn and make our industry better!

I am not sure how I totally missed this great article in DC Velocity entitled "Go Short" however I am glad I ran into it now. I think it is spot on and a great contrarian view from today's prevailing wisdom which is you need to be a "partner" in times of tight capacity. Partner generally is a euphemism for a trucking sales person asking you to give them above market rates to secure some nebulous and not guaranteed insurance policy for capacity in the future.

As this article rightfully points out, this guarantee is anything but that and generally will not stand even after you paid that insurance policy cost. The article states:

"At the heart of the study's findings is a fact that most who ship and haul for a living already know: that no truckload contract, regardless of duration, can force a shipper to honor a volume commitment, or a carrier to honor a capacity commitment. Because trucking is considered "derived demand"—meaning supply doesn't react unless demands are put on it—a carrier can easily change capacity, and the rate it charges, if it doesn't secure enough high-yield freight on a lane and finds better opportunities elsewhere. In many cases, it will stop accepting freight on a lane altogether."

As prices in the market change and as your rates become "stale" the carrier can just stop accepting tenders. They will say to you their "network has changed" and they can no longer support this lane. It happens all the time and it happens with the best and most ethical carriers. I am not accusing them of malpractice but rather I am just accepting what is and this article articulates it well.

This article advocates going shorter on your bid cycle, perhaps one year, and ensuring rates and lanes do not "get stale". Interestingly enough, despite all the discussion from the carrier base about "long term partnerships" this appears to be in their best interest as well.

It is important to outline another extreme which is highlighted in the article. Grough Grubbs, SVP of Distribution and Logistics for Stage Stores says:

"Our rating is dynamic based on competitive bidding, rather than an annual volume bid. This removes the dilemma of 'stale' bids," said Gough Grubbs, Stage's senior vice president, distribution/logistics. "As more competitive bids come in for certain lanes, incumbent carriers are given the opportunity to revise their rates in our system if they choose to. If not, they drop down in the pecking order for future loads."

This certainly looks and feels like every day is a new day and the bid cycle essentially never stops. While this ensures market prices every day you would need to identify the trade off of this strategy with the benefits of some sort of stability. That trade off equation would be different for each company and you would have to look at it in the context of your own competitive environment.

One of the concerns I have written about many times is the fear the coordinated industry effort to "scare" shippers by talking about capacity shortfalls and rising prices (a week does not go by where a CEO of a trucking company feels a need to "remind" us that lowering capacity will result in higher prices) would result in the industry actually reinforcing to shippers that this is a commodity business. Again, I do not believe it is a commodity however if all you talk about is the commodity behavior of the pricing scheme then you are essentially educating your customers to treat you as a commodity.

This article, and certainly Mr. Grubbs has taken it to the fullest measure.

Those who have been in the industry a while know the Council of Supply Chain Management Professionals (CSCMP) is the premier professional organization for our industry. From practitioners to academics, this is the organization to belong to if you want to know what is happening in our industry, networking with top individuals / thought leaders and keep an eye on the mega-trends occurring in supply chain and logistics.

This year I have the honor to co-host Track 6 - Energy and Infrastructure at the Annual Global Conference in Atlanta from September 30 to October 3. This track will have exciting discussions concerning the overall energy marketplace right to how to specifically implement Natural Gas and alternative energy strategies. The track objectives, as stated in the program:

"Managing a sustainable supply chain is no longer just a "cool" thing to do; it is expected by the consumer and is an extension of the brand and product being sold. This track will highlight best-in-class practices and emerging technologies to reduce your carbon footprint, enhance your corporate image, and positively impact the bottom line"

I highly encourage you to put this on your appointment calendar!

Today, I will highlight the first session we will have which is from 9:45 to 11:15 on Monday, October 1, 2012 entitled: Dispelling the Myths of Energy Independence by Walter Zimmermann, Senior Technical Analyst, United ICAP. The description of this session is:

"US energy independence is a goal that can never be achieved due to the global nature of the economy and the ability to export energy quickly to the higher priced markets. There is a lot of talk about building a stronger economy while at the same time lowering energy prices. This speaker will explain why we can’t have both, and why the financial markets are what actually drive energy price trends. He will reveal what can be done to lower energy costs, and describe how seasonal price cycles can be employed to lock in prices near their annual lows."

This will be an exciting session as it will challenge a lot of the current thoughts which exist in our industry about how we are on the beginning of a wave of cheap energy and energy independence. Mr. Zimmermann speaks how the laws of supply and demand are not driving fuel costs but rather the "financialization" of the energy markets are really driving the costs. This session will really challenge you to think different.

Mr. Zimmermann is an exciting and dynamic speaker which will make this session very exciting. Bring your questions!

If you would like to see him in action, take a look at this clip from CNBC:

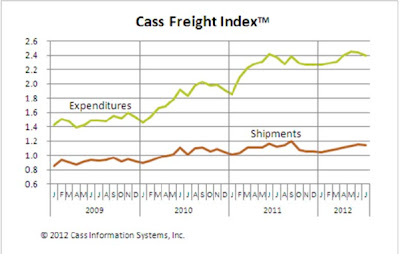

The Cass Freight Index is out for August and the results are not surprising for those of us who stay close to this market every day. Both expenditures and freight volumes have decreased month over month in August signaling a dramatic slowdown and one during a time when some would expect the seasonal surge to start. Remember the idea of seasonal surcharges?

Cass Freight Index

Year over Year and Month over Month, shipment volume has decreased 1.1%. For expenditures, we are still up year over year by 3.8%, mostly driven off of irrational fear instilled in the market during the first quarter (the reality was there was no need for those rate increases however some bought into the fear driven by some industry leaders) but month over month the expenditures are down 1.1%. Some other points made by the people at Cass:

There have been two straight months of freight contraction

This is the third time this year, freight volumes are down year over year

Inventory levels are increasing beyond what is needed for the sales volume in the economy.

The report says to expect rates to stay firm - I disagree with this and I think the empirical evidence will show this not to be true.

The report continues to say driver pay and fuel is driving higher costs for the carriers. Of course, we know higher fuel costs are burdened on the shipper, not the carrier, due to fuel surcharges. I also have not seen a massive increase in driver pay however we shall see if that starts creeping in. The report says these increased costs have not made it through to the shipper in rates however the long term trend is the costs are passed on. The average operating ratio (OR) has decreased (margin increasing) for the better part of a year now. This means either the carriers are getting great operational efficiencies to offset these cost increases (that would be a good and competitive thing to occur) or the costs are being past through. Impossible for the carrier costs to increase and the OR rate to decrease without one of the two above occurring. As always, it probably is some of each.

So, here are my thoughts for shippers:

Despite a somewhat coordinated effort across the industry to reduce capacity it appears demand is decreasing even faster. This is a message I have been projecting for the last 6 months and the evidence here continues to reinforce this general message.

If you are a shipper who was frightened into taking increases at the beginning of the year you may want to review that decision and perhaps run a bid event. You most likely are paying out of market prices.

The idea that Q3 and Q4 is a bad time to bid may be an idea which is dying. Carriers should be worrying about where the volume in Q12013 will come from now and may be a bit hungry.

This report continues to reinforce the incredible volatility of the market and the fact every shipper needs to have a very detailed supply base management program to monitor these changes and leverage them when needed.

For carriers I believe:

May be time to stop a lot of the blustering and start building true relationships with your shippers to lock in shrinking volume. Getting business out of fear is not always a good or defensible long term strategy.

Offer value added services to ensure you bring more than just transport to the mix. Shippers need overall logistics and supply chain partners to make it through slow times.

Continue to drive exceptional efficiencies. As an industry we need to ensure that logistics expenses as a % of GDP declines. That is the true measure if our industry is adding value or not. Let's focus on the right things.

Continue to drive hard for increased fuel mileage and sustainability objectives. This benefits everyone.

In conclusion, the signal this report is sending is things are slowing down and the pace may be accelerating. Get ready for a tough Q42012 and Q12013.

I find just about everyone gets the idea that putting more stuff in a trailer will generally reduce your overall costs because you will use less trailers. It is that simple. Miles per unit sold goes down and with that the cost of transportation. Further, your sustainability goals are met far quicker because less miles means less emissions. The easiest way to reduce the cost of anything is just to stop using it. Concentrating on cube utilization accomplishes this.

However, for all the people who know this I find a lot less worry about secondary cube or what some call "liquid cube". This actually takes into account the utilization of the cartons or packaging of product you are loading in the truck. Think of it this way: You may load 1,000 cases of xyz product into your trailer, look at it, and say "wow, did I cube out that trailer"! What you may miss though is the cube utilization of the cases is horrible. Open the cases and you may find a lot of air due to bottles being curved, sizing relative to the case not done properly, or just packaging which is too big for its contents. If you are able to solve that problem (per my previous post, most likely with the marketing and merchandising folks) you may find you can put a lot more product in that same trailer.

So, the journey continues... Once you think you have cubed the trailer, start looking at secondary cube and start solving that problem. Keep packing them tight and ELIMINATE emissions and cost; don't just reduce it.

(Answer to above question: A lot more would fit in a trailer - after all, the rind is merely nature's packaging!)

Conducting what I call a "walk around" (my wife calls it shopping) in the grocery store this weekend started my mind wandering to ideas about packaging and shelf space. Why would a logistician be thinking of these stereotypical marketing and merchandising topics you may ask? The answer is simple: There is a battle going on in the retail world within companies and it is the battle of the logistician versus the merchandiser.

Just look at the picture below:

A merchandiser probably sees nice colors to attract the shopper's eyes, good shelf space display, multiple rows of the product to dominate the shopper etc. A logistician sees boxes which are too big for the product which is in them thereby reducing useful cube in a trailer. If you look to the far end of the aisle you will see round and curvy shaped bottles. The logistician thinks these attract the eye but kill you on cube (both primary and secondary) utilization. So, the question is who wins? To this point in my career the merchandiser has won but that is changing with three key changes in the external environment.

First, transportation costs have become so high people are no longer just deferring to the merchandiser. They really need to make a solid business case why that curvy bottle which kills cube utilization is going to drive sales. Otherwise, we will move to optimizing cube.

Second, shelf space is no longer such a driver of consumer preference. When the entire concept of shelf space importance was developed it was the way to advertise to an uneducated consumer. The consumer "learned" about your product by having the product catch her eye then have her read the box (another more practical reason why boxes are so big - need real estate for the writing and graphics) and this would be a major driver of her buying decision (The old adage there are two moments of truth: One when she decides to buy the product and two when she uses the product for the first time). However this has all changed. Many come to the store already knowing what they will buy as they have researched it prior to arriving. Or, if they have not, rather than read the box they will whip out their smartphone and read about it on line (the smart merchandiser will have a QR code on the box so it can be scanned). This is a mega trend for how people shop which is growing and not shrinking. The advent of the smart phone means you no longer have a self contained space to barrage the consumer with colors and splash - the consumer can "virtually" leave your space, find the information they want and need, then reenter your space without you even knowing it.

Third, as stores become smaller (especially if you follow the mega trend of consumers moving back to the cities which changes the entire dynamic of retailing) shelf space is shrinking. With shelf space shrinking you need to figure out how to get your product in front of the consumer, get it to be interesting AND make it small and compact (The tyranny of the "OR" - Good to Great, Jim Collins). For example, if you make laundry detergent and you only get 1' across on a shelf. You can take that up with two giant bottles of non-concentrated detergent or you can concentrate it immensely and get 6-8 bottles across. I personally believe more is better and the the signal the consumer will get is if there is that many on the shelf it must be because people are buying it - perhaps I should try it. This trend supports and is in harmony with the needs of the logistician.

So, what does this mean for the logistician? It means you need to get upstream in the packaging design, merchandising and manufacturing of your product. Get involved in these decisions on the front end and influence the decisions which will meet the needs of the marketer and merchandiser and will also play nicely with cube utilization and transportation costs. The lowest cost transportation is the transportation you do not use and better cube and better secondary cube (a topic I will address in another post) drives the elimination (not just reduction) of transportation cost. This means you need to be intimately involved in the Sales and Operations Planning (S&OP) process and if your company does not have one you should lead and develop one.

I have always said the great logistician spends as much time on these topics as they do on working with carriers. The work with carriers tends to be fun part however this is where the majority of your cost savings will come.

Our industry, the logistics and supply chain industry, should reflect more on this great day than just about any other industry. We are built on the benefits of the work labor does every day. The number of truck drivers, loaders at rail and air ramps, workers at ports, warehousemen etc. etc. really do drive this industry. I have not done the analysis however the ratio of labor (stereotypical "blue collar") to "management" or managers has to be one of the largest of any industry. Think of it, for every truck there is at least one driver!

This industry also is what moves America. Nothing is built, bought, imported or exported without going through some channel in this industry; and most go through multiple channels in our industry.

So, with that I do reflect on this great industry and the great people who work in it. I hope they get to spend time with their families - although the nature of the industry is many will not.

Thank you for all you do for your companies, this industry and the United States of America!

In deference to the great writing at Supply Chain Digest by David Schneider (David K. Schneider and Company) I will not rewrite the premise of the article he wrote over at SCD titled "The One Best Supply Chain Metric". I will only say I highly encourage you to click on the link above and go to the article and read it if you are even remotely interested in a different metric to follow.

Now, on to my opinion (hopefully you have linked over and read the article): Operating cash flow is a "king" metric or an "outcome" metric as some may call it. It is the ultimate scorecard. Are you truly making real money (i.e., Cash) or are you making "paper money" (through income statement shenanigans) and burning through cash? Remember, the only thing which allows you to reinvest in your business is the generation of cash. Measure cash in a big way.

I get very nervous when I hear companies want to "push out payables" not because I think it is just wrong to do but also because of the signal it sends which is their cash from operations is probably going down so they are grabbing a one time cash infusion from suppliers.

Ultimately, cash from operations will determine the success or failure of your business because ultimately you will run out of financing (of which pushing out payables is essentially that - you are financing through your suppliers) and investing options. When that happens, if you are not generating cash from operations, you will find your "Emperor has no clothes".

As if on queue from my posting yesterday, Mark Hulbert (read all his stories here) writes on marketwatch.com about the divergence between the Dow Industrial index and the Dow Transports. He shows a graph which is very interesting and may help answer the questions I raised yesterday when I asked how the economy (as measured by the stock market) could be so high yet freight growth appears to be crawling along. His graph (reproduced below) shows for some time now the Dow Transports have lagged the overall Dow. I suspect if you put in the S&P500 you will see this as well.

Dow Transports (in Red) Versus Dow

So, what does this tell us? Mark believes it may signify the leading indicator of an overall slowdown in the economy (which of course does not bode well for the transportation industry). However an interesting point which I had not followed before is his point around the divergence or the relative performance of the Dow Transports to the Dow overall.

He claims (as apparently it is in Dow Theory) that it is precisely this divergence which indicates the slowdown not specifically the fact that that transports are slowing down.

Perhaps it is best to think about it this way, like a good race horse, the Dow is executing one last gasp then it will stop where as the other race horse (i.e., the transports) already crossed the finish line and is stopped. I don't know if that is a good analogy or not however I will set a favorite to always compare the Dow transports to the Dow overall now and let's see how his analysis plays out.

The Cass Freight Index report for July 2012 was somewhat anti-climatic for those of us who follow freight and knew we were in the depth of the great slowdown of 2012. The "phone bank" report (which measures the direction of phone calls from a fictional transportation manager's desk) reported far more incoming calls from carriers looking for freight than outbound calls searching for trucks and this has been true for at least two months now.

OK, I admit that is not a scientific index however if you are close to the business and have a grasp on that general topic it is a highly effective predictor of freight.

Cass Freight Index - July 2012

We see from this index that essentially expenditures have leveled off really since June of 2011 with just a little bump at the beginning of Q2 in 2012. I attribute both years' early bumps as price / volume "hype" and not reality. Each of the last two years has begun with a "great hope" of where rates and the economy is going only to become disappointing by summer and a steadying of rates. A good and experienced transportation manager will see this trend and ensure they do not buy into the early year hype every year.

At the beginning of every year the transportation company sales people will show up with all sorts of data to tell you "this is the year" where we will hit a massive capacity crunch so you better "pay up now" to be taken care of later. A great story which makes for great industry journalism however the empirical evidence suggests it is, in fact, all hype and those who remain calm in the face of the story will be better off.

A key question though is how can all these companies (shippers) report great earnings, the market is very high ( Dow at 13,175.64 as of this writing) and yet the shipments and movement of goods is stagnant? I have a few theories (I freely admit these are theories however the data is showing this to be more and more true).

First, the economy is a more services and financial economy than it is a "things" economy. While we still consume the manufactured goods we generally do not make them. This means an entire portion of the former economy shipments is gone and that is inbound to manufacturing. The outbound is still there however the inbound is gone. The inbound freight is in China and Mexico and other low cost countries. Those who say they love being in trucking because their jobs cannot move overseas are wrong. The inbound jobs have moved overseas along with the inbound freight.

This of course follows the manufacturing base so if manufacturing truly does return to the United States (the jury is out on this) then the inbound will follow back.

Second, the great work on sustainability, minimizing packaging, routing efficiencies etc have all led to being able to move the same amount of goods with lesser number of vehicles. This movement is good for all of us in the world however it does decrease the raw demand for trucks. Just think of televisions. If the economy sells a million T.V.s this year (a made up number just to illustrate the point) they are all about 1" thick. 10 years ago if 1 million T.V's were sold they all were about 3 feet deep (packaged). That is a lot of trucks.

There is not only minimization of the product size but there is also the elimination of the physical product (think e-books. iTunes for CDs etc.).

So, my conclusion is you cannot compare the GDP numbers of today relative to prior year GDP numbers as if there is a straight correlation between the level of GDP and the amount of goods moving in terms of cube size (which is the driver of number of boxes needed). Clearly there is some kind of correlation but it is not as direct as it would have been 10 - 15 years ago. The economy can grow with less physical product moving.

Finally, the lesson learned of the last two years is clear: "Be Not Afraid"! at the beginning of the year. Don't buy the hype, be patient, watch the data and let the economy play out. You get no credit (regardless of what the sales person tells you) for being an early mover on rate increases.

I have read a lot recently about how you get the real GDP numbers out of China. Don't bother with the government statistics rather just go look at the piles of coal at the electric power plants. As China has said their economy is doing fine, observers of coal piles have seen them grow and grow. Why is this important? The growth of the coal piles signifies a massive slow down in the demand for electricity which, in turns, means factories are idling. When factories idle, you have lower GDP. Voila! It may not be scientific however doing econometrics with raw data which is flawed is a waste of time.

So, I thought I would use this way to look at transportation and I did not like what I saw. Driving through Chicago yesterday passing by the big intermodal yards I saw stacks and stacks of 53' containers which clearly had been "mothballed". They were not at the yard "in transit" rather they were in the yard and parked. They were stacked high and tight. This indicates carriers are parking containers which clearly indicates a massive slowdown in freight pretty close to the time where it should be gearing up for the holidays.

All indications are the economy has softened dramatically and this is just another indicator. I may patent this methodology, go to Chicago every week and take a picture, compare them against previous weeks like you would a bar graph. My guess is this would be just as good as some of the other "analysis" I have seen.