During holidays I really like to spend time with a good book and this Thanksgiving was no different. I am reading (and re-reading) Clayton Christensen's book: How Will You Measure Your Life? This book is a fantastic read and it uses models of operation to help guide you in both your personal and professional life. I may call on this in future postings but today I want to discuss his chapter on selecting talent called: The Schools of Experience.

In this chapter, Professor Christensen discusses how one should look at their careers and subsequently how someone should look at hiring talent. The old model of climbing a ladder is no longer useful in a "flat" world (using Thomas Friedman's analogy and applying to corporate America). Most organizations are extremely flat - especially relative to years ago - and this means it is a collection of experiences which will both drive your career and should drive your selection of talent. He has many examples but let me provide two from my own career:

Transition from the Military:

The military was a fantastic place to both give back to the Country and also to accumulate many experiences: Leadership, operating in stressful environments, fast decision making, and I could go on. Truly, I cannot imagine any civilian business giving better experiences at those situations than the military.

However, the military does not provide a lot of financial experience, profit and loss experience or business competition experience (There is, after all, only one Pentagon!). So, when the opportunity presented itself, I moved into the business world. In that world I have experienced all the items I mention above. Was it a "promotion"? If measured by wages, true cost of living, or titles it could have actually been considered a demotion. If measured by gathering huge experiences which I could not get in the military, it was a huge promotion!

Transition from "Big Company" to Entrepreneurial Company:

The skills required to work in a big company with large well established processes are completely different than those required in the small and entrepreneurial world. So, using the theory of "experiences" I decided I wanted that small experience even though I was in a well established executive position at a great company.

Using supply chain metrics, was it a promotion? I went from managing 14M square feet of warehouse space to 6M square feet. I went from $300M+ of transportation spend to $80M. To the stereotypical person, this could be seen as a "lesser role". Trust me, it was not!

I quickly learned the skills used in a large company are close to useless in a small, everyone does the work, entrepreneurial and "scrappy" company. The experiences I gained at this smaller company could never have been attained in the larger, well established company. And, if I were to just do what I did in the large company in the entrepreneurial company, I would have failed. I had to adapt, learn, gather new experiences and apply them to the unique issues.

What does this mean for talent acquisition:

Even today with the sophisticated human resources (HR) departments I still find people rely on the "ladder" model versus the "experiences" model. For example, if you were hiring for a start up company would it matter that someone become a SVP in a multi-billion dollar company? That person has incredible experience (and has been successful) in delegation, building staff, using sophisticated ERP such as SAP etc.

What this person lacks is start up skills. Can they do a lot of the work themselves? How will they perform without "staff"? Etc. The "ladder" model shows that this person is a great pick but the "experiences" model shows the person to be lacking in a number of major areas.

Conclusion:

We can use the "experiences" model to guide both our careers (choose experiences over perceived promotions) and we can use it in talent selection. It tells a different story when this is applied versus the "ladder" model. My advice for those starting their careers is to work to get many different experiences and work to stitch together a set of skills, acquired by experiences, that will serve in you in a multitude of settings. This will ultimately serve you better than "climbing the ladder".

A 25 year veteran of the supply chain and logistics industry blogs on all things logistics. Experience in 3PL, automotive and consumer goods logistics help bring a unique insight to this topic

Sunday, November 27, 2016

Friday, November 25, 2016

The Amazon Effect

For anyone who runs a warehouse and has Amazon "come to town" you know, at a very micro level, about the "Amazon Effect". The entire labor and transportation capacity situation in your town changes in an instant.

However, it is bigger than that from a nationwide perspective and I had the privilege of listening to a very insightful presentation given by Eric Johnson (Twtr: @AmShipEric), research director and IT editor at American Shipper at the Jacksonville CSCMP roundtable event in October.

He had some very good insight into what Amazon is trying to become and what they are not trying to do. My conclusion, after listening to Eric, is Amazon wants to "own the customer". Now, of course the key question is what does this mean?

If you think about "owning the customer", it really covers about 5 major touch points:

However, it is bigger than that from a nationwide perspective and I had the privilege of listening to a very insightful presentation given by Eric Johnson (Twtr: @AmShipEric), research director and IT editor at American Shipper at the Jacksonville CSCMP roundtable event in October.

He had some very good insight into what Amazon is trying to become and what they are not trying to do. My conclusion, after listening to Eric, is Amazon wants to "own the customer". Now, of course the key question is what does this mean?

If you think about "owning the customer", it really covers about 5 major touch points:

- Own the order experience (The first point to gain loyalty for any product). This drives all sorts of information technology.

- Own the delivery experience (Appointments, delivery, right to how the customer is greeted).

- Own the post delivery experience (solve issues etc)

- Own the payment experience (whether they sell it to you or not).

- Own the customer ecosystem (Alexa app, ECHO and DOT).

If your company is not investing heavily in all of the above you most likely are going to be displaced by Amazon at some point. This is why I published: "What Exactly is Amazon... 3PL? Retailer? IT Company? Delivery Company? - Answer: All of the Above" back in October of 2015!".

Bottom line: The story has not changed. Amazon is coming for your business regardless of what you are doing so be ready to compete. And, for those who think it is just a matter of time before they are crushed by the weight of costs, think again. They have entered into a new space and as this article from back in February reminds us: They are winning the race for the smart home, and no one is noticing.

October Results are Not encouraging for Transportation Providers

It may not be a complete "Happy Thanksgiving" for people who manage 3d party transportation. After some very large decreases in the last few months, the CASS Transportation index decreased again in October. The transportation index dropped 1.4% in October. While this is better than the drop of 2.8% in August and 3.5% in September, it still shows that there is over capacity in the transportation industry.

The Intermodal index rose, YoY for the first time since 2014 by 0.4%. This, I would call a "rounding error". Let's call it flat.

As I have discussed for many years, there is a fundamental shift in the way freight is moved in the US and I am wondering if even the metrics are wrong? Should we be so tied to this freight index and does this really tell us about the economy? Today, the economy seems to be moving fairly well but transportation continues to decrease. The issues:

The Intermodal index rose, YoY for the first time since 2014 by 0.4%. This, I would call a "rounding error". Let's call it flat.

|

| Source: CASS Transportation |

|

| Source: CASS Transportation |

- Miniaturization of product

- E-Commerce (reduction of movement of product to stores

- Digitization of product - more product delivered electronically (Books, newspapers, inserts, music etc.).

- Localization of suppliers - This is very interesting because it is a function of transportation costs getting out of control a few years ago. As more finished goods / component mfgs localize, transportation requirements decrease dramatically (Better cube utilization when shipping raw materials v. shipping finished goods or components).

- The Borrowing Economy: I will write more about this and the impact to supply chains but this is real and it is impacting how much we buy. Think about how many items you have that sit and do nothing most of the time. If people start aggregating this in a borrowing economy, the total amount of product bought and shipped will be reduced dramatically.

Tuesday, October 25, 2016

Marc Althen at Penske Logistics - Leading by Example and Empowerment

A great article about a great leader titled "Leading by Example and Empowerment". Congratulations to Marc Althen.. .well deserved

Monday, October 24, 2016

CASS Report from September is Somewhat Grim - Macroeconomic Monday

OK, I am late to the party on this one, sorry but when I read it I thought I had to write, albeit, late. The Cass Freight Index Report from September had virtually no good news in it. The best thing they had to say was (actual quote), "... the YoY contraction [in expenditures] appeared to be less bad [than August]". When all you can say is "It is not as bad as last month", you know it is bad.

On To the Numbers:

On To the Numbers:

- Shipments were down 3.1% YoY

- Expenditures were down 3.8% YoY

And the industrial recession is on. I think they rightfully state that the culprit may be the contraction in inventories. I have written many times about the growth in inventory relative to sales and I think companies have realized they need to get rid of those inventories. This means most product is already here and in the warehouses / stores and this reduces the need for transportation immensely. Why buy new product when you are so dramatically overstocked.

|

| Destocking takes bps out of GDP |

This graph, from CASS, tells the story that destocking, while slowing down, is still a drag on the economy. CASS says they are continuing to be concerned about too many autos, elevated inventory relative to sales and the fact that the consumer has not really dove in with both feet (or open wallet).

Now, the key issue will be whether the Fed increases interest rates in December as everyone expects them to. That will be a real problem as the economy, even if you think it is good, is truly running on just about one cylinder.

What does this mean for shippers and providers:

I think the data is clear, and has been for at least two years now, and it is telling us that the shippers are in control (especially in ocean freight) and will be for the foreseeable future. Of course, this is nothing to write home about as this means the economy is soft. However, if you are shipping and you have a nice business you should take advantage of these soft times. Believe me, when it swings, you better duck. And, as all my readers know, you will not get benefit because you overpaid in a slow environment.

Actions:

- If you have not bid freight in a while - do it now.

- Lock in rates for two years if you can - a nice hedge

- Move to a market based fuel system to take out any fuel fluctuations in the rating structure

- Watch tender turn down rates. This will act as a great "early warning" telling when / if the tide turns (don't expect this until 2018)

Sunday, October 2, 2016

An Update on Drones and Drone Delivery

I wrote about Drones first in February of 2013 after watching a Nova episode called "Rise of the drones". This was almost a full year before the infamous Jeff Bezos 60 minutes episode where he somewhat stunned the world discussing using drones as delivery vehicles. In one way we have come a long way and in another, it is amazing how slow it has taken to commercialize this.

Two updates to report. First, at the CSCMP Annual Conference I was able to attend the "Educators Conference" and watched a great presentation by Professor Dr. James Campbell, Professor and Chair, Logistics & Operations Management Department, College of Business Administration, University of Missouri - St. Louis. He discussed the use of the "Truck - Drone" hybrid which entails trucks moving to central locations with product. At that location, the drones would be launched and conduct deliveries. A fascinating topic which made more sense as things such as battery life and laws about flying out of vision will make launching them from central DCs almost impossible for the near term.

He also had a nice graph showing the cost per delivery and Amazon can get this cost down to $1.00 per package. That is amazing. There was a lot more in the presentation and it is clear thought leaders such as Dr. Campbell are making large strides.

Second, I checked in on Missy Cummings who, in 2013 was the star of the Nova episode. Remember, she was one of the first F/18 pilots for the US Navy and a graduate of the US Naval Academy. She now runs HAL - The Human Autonomy Lab at Duke. She continues to study the use of bigger and bigger drones and believes these will be used for delivery. She also has an interesting twist (See video below) on the human interaction of drones. That is becoming the topic as the technology is no longer "futuristic" but rather it is known and can be implemented. The question is how will we interact with drones.

If you have not seen the original NOVA episode, even though it is 3 years old, you really should watch it (Below). I have also included a recent speech Missy made. She is truly brilliant in this field.

Two updates to report. First, at the CSCMP Annual Conference I was able to attend the "Educators Conference" and watched a great presentation by Professor Dr. James Campbell, Professor and Chair, Logistics & Operations Management Department, College of Business Administration, University of Missouri - St. Louis. He discussed the use of the "Truck - Drone" hybrid which entails trucks moving to central locations with product. At that location, the drones would be launched and conduct deliveries. A fascinating topic which made more sense as things such as battery life and laws about flying out of vision will make launching them from central DCs almost impossible for the near term.

He also had a nice graph showing the cost per delivery and Amazon can get this cost down to $1.00 per package. That is amazing. There was a lot more in the presentation and it is clear thought leaders such as Dr. Campbell are making large strides.

Second, I checked in on Missy Cummings who, in 2013 was the star of the Nova episode. Remember, she was one of the first F/18 pilots for the US Navy and a graduate of the US Naval Academy. She now runs HAL - The Human Autonomy Lab at Duke. She continues to study the use of bigger and bigger drones and believes these will be used for delivery. She also has an interesting twist (See video below) on the human interaction of drones. That is becoming the topic as the technology is no longer "futuristic" but rather it is known and can be implemented. The question is how will we interact with drones.

If you have not seen the original NOVA episode, even though it is 3 years old, you really should watch it (Below). I have also included a recent speech Missy made. She is truly brilliant in this field.

Mary "Missy" Cummings Gives Talk at Duke

PBS NOVA - Rise of the Drones

Sunday, September 18, 2016

A Balanced Summary of Where The Trucking Industry Stands

Fleet Owner summarized the FTR Transportation conference with an article about the headwinds facing the transportation industry. They are real but they are what every business faces - uncertainty. That is what makes a business a business. Certainty is what utilities have.

Usually the press out of this conference is designed to scare the shippers into paying higher rates than they need to but, at least within this summary, it appears they are becoming more realistic. Here are some key points:

Usually the press out of this conference is designed to scare the shippers into paying higher rates than they need to but, at least within this summary, it appears they are becoming more realistic. Here are some key points:

- 2% GDP growth for the next two to three years (A number I have used for many years now). This is significant because virtually all the transportation executives I know say the real capacity crunch comes at 3% GDP growth.

- Eric Starks states the industry will flat in the foreseeable future. Flat means leaders tend not to know what action to take; what bet to make.

- Mark Rourke, President of Schneider claims they have a 4% to 5% productivity decline due to electronic logging devices (ELD) and they have not recovered from this since. This I will never understand and wish someone would explain. How can ELD's cause a productivity decline unless you are not already following the Hours of Service (HOS) laws. I would think this would make them more competitive as it will ensure everyone follows the laws.

I also think one of the biggest issues facing the trucking industry is just the nature of the "new freight". With freight now going to central and very large DCs and then parceled out to the consumer, the entire leg of freight going to the store is being eliminated. Think of this: Rail gets it to the DC and the part that was truck (DC to Store) is being eliminated. As leases run out, more and more retailers will close stores and go to on line. This will have a huge impact to the trucking market.

Perhaps this outlook (grim as it is) is what is driving the Schneider IPO?

Saturday, September 17, 2016

Schneider Seeking IPO

A fascinating development from the Frozen Tundra. I just read they are seeking to do an IPO for part of the company. I was there when they did this the last time... It crashed and never happened. Let's see what happens now.

More evidence that I think the Schneiders want little to do with trucking. Don Schneider used to say the decision to go public was only a finance decision to get access to capital. In this day with interest rates as low as ever and with free money everywhere, one wonders why you would go public now. It cannot just be an "access to capital" question.

Tuesday, August 30, 2016

Fundamental Supply Chain Shifts Kill The Idea of a "Surge"

I have talked a lot about the inventory to sales ratio and how it is such a great predictor of what will happen in the transportation industry. Back in April I was sending a warning sign in my post "Inventories Continue to Grow" and I even signaled this all the way back in 2012 in a post titled "Inventory to Sales Ratio Tells A Grim Story". It appears the Wall Street Journal now agrees.

In an article today titled "At Ports, A Sign of Altered Supply Chains", they discuss the muted growth (or at least not shrink) of the trucking and ocean business. The cause? You guessed it - the fact that inventories are high, the consumer is moving to on line purchasing, and the more disciplined approach to inventory management. There are some key shifts happening:

In an article today titled "At Ports, A Sign of Altered Supply Chains", they discuss the muted growth (or at least not shrink) of the trucking and ocean business. The cause? You guessed it - the fact that inventories are high, the consumer is moving to on line purchasing, and the more disciplined approach to inventory management. There are some key shifts happening:

- Demand Sensing Supply Chains: These have finally come into their own. Companies are much better at identifying the purchase trends and immediately shifting inventory purchases to adjust. If the consumer slows (or moves from apparel to electronics for example), Demand Sensing Supply Chains adjust almost in real time. Gone are the days of huge inventory buys "just in case".

- On Line Purchases and The Death of Excess Inventory: Anyone who has managed inventory knows these key tenets of inventory management: As you move inventory out and disperse it among stores or other storage points, your forecast accuracy decreases, your errors increase and the likelihood you will "orphan" inventory in the network increases dramatically.

To solve these gaps in information, you generally overbuy inventory to keep "in stocks" high.The inventory benefits of on line are clear: Far fewer inventory points (probably 4 at most) result in much higher accuracy which translates into far fewer inventory dollars to service the same consumer base. This, of course, translates into much less transportation needed. Those who say it does not matter, we are selling the same amount of stuff, do not know how the "laws of inventory" work. - The Growth of The Supply Chain Data Scientist: This is an entirely new field in supply chain and is different than just being an analyst. This is deep diving into data, pulling "fuzzy" data points together and identifying trends. These people see changes in buying patterns far earlier than ever before and provide that information to management which responds far faster than ever before. Inventory buys can be shut off in a nano second.

These factors are resulting in a far more disciplined inventory management process. We have been in an "over inventoried" position, in the aggregate, for a very long time and I have been predicting this will keep the demand for transportation services muted. This is what is happening.

Source: Wall Street Journal

Wednesday, August 24, 2016

The New Transportation Technology Ecosystem is Shaping

Developing the future is messy. It always appears it cannot be done and individual technologies, when looked at in isolation, look like they will never work. However, I submit this is short term and to borrow a Star Trek phrase, is "Two Dimensional thinking". Let's think about this in "three dimensions - think about the ecosystem and the connection of this ecosystem.

Let's review some key technologies being developed or deployed now:

Let's review some key technologies being developed or deployed now:

- Electronic logging

- In cab cameras that go beyond just filming but rather sends signals to centralized managers who make real time decisions.

- "Uber" type applications for booking, managing, and tracking freight

- Autonomous vehicles and the "Otto" type technologies.

- On line immediate economy (hour type delivery)

All of these technologies have advocates and enemies when looked at in isolation. However, I submit that you have to think of this in "three dimensions"; you have to connect the dots. All of these technologies need to come together to build the infrastructure of the future for transportation. They all point to one thing: A driverless truck.

The core to this is the autonomous vehicle - which probably explains why Uber buys Otto. But then, once this is solved, there are other things that have to come into place for this new ecosystem to work: You have to book the freight easily (enter Uber), you will want to see what is happening (especially at delivery and pick up points) (enter cameras), you will need to track where the truck is and what it is doing (enter E-logging).

The one thing I cannot figure out is how the truck will fuel and perhaps that leads to a futuristic truck stop which caters to the autonomous truck. Perhaps the biggest issue with this entire ecosystem is how will the truck stops like Pilot make money when there is no one to go into the C-Store to buy stuff.

So, when you look at the entire ecosystem of the future, you can see it taking shape, albeit messy, with all the technologies being developed. If you look at them in isolation, solving an old problem (i.e., Does E-Logging really solve driver logging or does it prepare us for having no driver?) then you will wonder "why do we need this". If you look at them together, building the new transportation ecosystem, then you say, "Got it!".

Those who look at these developments individually make me think of Khan and his two dimensional thinking:

Will The On Demand Economy Work in For Hire Freight?

I recently read a very well written article in Trucks.com titled: Will The Sharing Economy Disrupt Trucking, Transportation and logistics? It covered the very common topic of the day which is the "Uberization of trucking". Will it work? Can shippers get over the fear of people they do not know actually hauling their freight? Will it be consistent enough for commercial customers?

All of these questions are great questions and I have always said that all the answer to these questions are simple: Yes, it will be messy during the transition; Yes, these issues will all be solved; and Yes, the ultimate solution will not look exactly like we think today but we will move more towards "Uber" than we will stay where we are.

I think this is generally the conclusion of the author however I disagree with him in one major aspect: He still thinks of logistics in isolation of everything else that is involved in getting products to market. He says:

Think of the significant advantage in cost/sqft on line retailers have relative to those who have to get high cost real estate in commercial locations. The bottom line is there is a total cost to deliver product from the raw materials, through manufacturing, through distribution and the finally, delivered to the customer. This cost has to be looked at in its entirety and you cannot just look at one element and say something will not work due to the cost of that one element. If other costs are reduced or eliminated then perhaps that final mile cost can go up a bit.

Finally, don't think that this is a "law of physics" cost structure as this author thinks. Once you say "law of physics" it becomes a discussion where one believes the costs cannot be mitigated:

Finally, don't think that this is a "law of physics" cost structure as this author thinks. Once you say "law of physics" it becomes a discussion where one believes the costs cannot be mitigated:

Well, along comes Uber buying Otto. And, that, as they say, changes everything!

All of these questions are great questions and I have always said that all the answer to these questions are simple: Yes, it will be messy during the transition; Yes, these issues will all be solved; and Yes, the ultimate solution will not look exactly like we think today but we will move more towards "Uber" than we will stay where we are.

I think this is generally the conclusion of the author however I disagree with him in one major aspect: He still thinks of logistics in isolation of everything else that is involved in getting products to market. He says:

" But for all the speed and mobility an evolving new model like this brings, there are tried-and-true, iron-clad laws of physics, geography and time that need to be respected by newcomers to the industry."This hints that the author thinks of the final delivery in isolation but in reality this is just one part of the overall cost. For example, what if the lack of retail space, the lack of moving product between nodes in a distribution network saves significant dollars. Some of those dollars are reinvested in a higher cost "final mile" solution and some are retained: The net new cost is less than the old cost.

Think of the significant advantage in cost/sqft on line retailers have relative to those who have to get high cost real estate in commercial locations. The bottom line is there is a total cost to deliver product from the raw materials, through manufacturing, through distribution and the finally, delivered to the customer. This cost has to be looked at in its entirety and you cannot just look at one element and say something will not work due to the cost of that one element. If other costs are reduced or eliminated then perhaps that final mile cost can go up a bit.

Well, along comes Uber buying Otto. And, that, as they say, changes everything!

Monday, August 22, 2016

1.4 Million Supply Chain Workers needed - Strategy: Keep the Ones You Have

Get ready! The "War on Talent" is here and it is here to stay. Fortune published an article titled "Wanted: 1.4 million new supply chain workers by 2018". We have always discussed the need to develop and nurture talent and now it is getting even more important.

If you are not focusing on how to develop and retain your great talent, you will be forever out in the market trying to recruit new talent. And that, most often, is a loser's game. It is much easier to develop what you have then try to assess and acquire what you do not have. Here are some of my ideas on how to deal with what is becoming a hyper competitive market for talent:

If you are not focusing on how to develop and retain your great talent, you will be forever out in the market trying to recruit new talent. And that, most often, is a loser's game. It is much easier to develop what you have then try to assess and acquire what you do not have. Here are some of my ideas on how to deal with what is becoming a hyper competitive market for talent:

- Cater to Millennials while at the same time ensuring the "gray hairs" experience is utilized. I hear a lot about the catering to millennials so I will not rehash this. I do think though companies have to ensure the more experienced workers have a place. These people carry years of ideas, experiences and knowledge. Combine that with the skills of the millennials and you have an unstoppable force.

- Be customer centric and dare I say - Customer Obsessed. People love working on customer focused ideas and activities. People want to grow businesses. People hate cutting and they hate shrinking. Be customer obsessed.

- Make if fun. I once had a boss who on day one showed me the company values and he actually went out of his way to tell me that "fun" is no where to be found. "This is a business", he said. it was that moment, day one, that I started to think this was not going to end well. People have to enjoy what they are doing. When you hear people say they are "passionate" what they are really saying is they love the blending of their skills and they are having fun using those skills.

- Invest in your people. If you do not, someone else will and they will be gone. Yes, you will have the few times where you send someone to training and they promptly leverage that into a better job somewhere else. But, don't make everyone who is left pay for that. Invest, invest and invest.

- Embrace the "boomerangs". This is a unique and interesting idea. Many companies will not entertain bringing a person back who leaves. I say you should embrace them. Think of it as an opportunity to say they looked, the grass was not greener and we are welcoming you home. That will go a long way for your current employees, who probably still have a loyalty to this person and I believe you will have gained an employee for life. They will have left, learned a lot and now come home. What great way to acquire talent!

I am sure there are more you may have but just like the easiest customer to get is the customer you already have, the easiest great employee to get is the one who sits right next to you.

Adding to this is an article by Tisha Danehl titled How to Recruit Top Supply Chain and Logistics Professionals. She has all the right ideas!!

Adding to this is an article by Tisha Danehl titled How to Recruit Top Supply Chain and Logistics Professionals. She has all the right ideas!!

Sunday, August 21, 2016

What Have We Done to The World?

Recently I posted about socially conscious and responsible sourcing. Michael Jackson says it much better than I:

Inbound Logistics Discusses Cost

As if on queue, after I wrote my article about recasting your discussion from "cost" control to "revenue" generation, Inbound Logistics published an article titled: "Keeping an Eye on Cost Management". The article discussed the 80/20 rule where 80% of a network's cost is baked in to the network design and 20% is about execution. I agree.

But, again, I must say the article totally misses the point of Customer Centric Supply Chains. You do not design your network to cut costs! You design your network to provide incredible service to your customers. Once that is done, you figure out how to do it at the most optimal cost.

Most of the work in network design is working cross functionally with sales and strategy to identify not only what customer needs are today but where will they be in 10 years. Where is the ball going.. not where is it today.

This is why Amazon is so brilliant in their supply chain strategy - they focus solely on the customer needs, they design to those needs and then they drive out cost. Further, they are not looking at the needs today but rather the needs 5 and 10 years from now. How do I know this? Easy: Everything Amazon does is first met with disdain, "no one can make money doing that" type statements etc. When I hear that, I know they are on to something.

But, again, I must say the article totally misses the point of Customer Centric Supply Chains. You do not design your network to cut costs! You design your network to provide incredible service to your customers. Once that is done, you figure out how to do it at the most optimal cost.

Most of the work in network design is working cross functionally with sales and strategy to identify not only what customer needs are today but where will they be in 10 years. Where is the ball going.. not where is it today.

This is why Amazon is so brilliant in their supply chain strategy - they focus solely on the customer needs, they design to those needs and then they drive out cost. Further, they are not looking at the needs today but rather the needs 5 and 10 years from now. How do I know this? Easy: Everything Amazon does is first met with disdain, "no one can make money doing that" type statements etc. When I hear that, I know they are on to something.

Sunday, August 14, 2016

Why Logistics' Leaders Need to Recast "Cost Control"

The best presentation I have seen in a long time was given last year at the CSCMP Annual Conference and it was given by Amazon. The topic was a general update on their supply chain however a statement was made that has stuck with me. The speaker was asked how they decide what service to provide given the costs. His answer was clear:

" We don't trade off. We provide the service then figure out the cost".

This is the definition of a true customer centric supply chain. The customer decides the service level and Amazon provides it. It is then up to the logisticians and engineers at Amazon to figure out how to do this profitably.

When the cynics asked him how long he can go with losing money, his answer was "We make a lot of money, we just choose to reinvest in the business". Another great answer and given the results of Amazon in the last few quarters, I think this issue of them making money has been put to bed.

So what is a person to do who is stuck in an "old school" business where the executives believe the only thing a logistician should do is cut costs? Here are a few ideas:

1. Recast it into growing revenue. Logistics systems, when planned properly and executed at a high level do more to grow revenue than most parts of the business - including sales and marketing. If you own the final mile of the delivery then you definitely have more impact.

2. Invest in quality. Why do I do almost all my shopping at Amazon? It is because the quality is near perfect and it is incredibly consistent. This, again, will grow the business.

3. Invest in final mile and own as much of it as you can. Amazon is learning that now with the various ways they are investing in the final mile for Prime. You can have partners but they have to execute your system. For example, Amazon delivers on Sunday through the US Postal Service. However, they use the exact same customer service alerts as any other part of Amazon. It is seamless to me as a customer.

I heard another person talk a while ago and it was about the two major touch points for a customer. These are the point of purchase and the first point of use. Because so much is moving to an order and deliver method of buying, the point of purchase for delivered goods is now both the on-line experience and the final mile delivery. Make the final mile great.

Of course, there are other items but these are the big three in my book. Do this and you will make your logistic's systems revenue generators and not costs to be cut. If your leaders do not see this, then start planning an exit strategy because they will ultimately lose in the market place.

Monday, August 1, 2016

Cass Indices for June Report Real Issues with Trucking and Intermodal

The Cass Indices for June reported what observers knew was to be the case: Once again the trucking "recovery" has stalled and capacity exceeds demand. Part of this is due to the elevated inventory levels with retailers and part just due to increased capacity. Remember, items are much smaller today then ever and with advances in packaging, the trucking industry just has too many assets chasing too few loads to sustain a lot of pricing.

For the last three months, the truckload index has decreased 2.3%, 1.2% and 1.8% respectively and the graph shows how difficult this market has become. We now are looking into 2017 before there is any tightening of capacity and pricing. I believe capacity will need to exit the market as not only is there too much today but the economy will start slowing and that means just the normal cycle would require removal of capacity.

For the last three months, the truckload index has decreased 2.3%, 1.2% and 1.8% respectively and the graph shows how difficult this market has become. We now are looking into 2017 before there is any tightening of capacity and pricing. I believe capacity will need to exit the market as not only is there too much today but the economy will start slowing and that means just the normal cycle would require removal of capacity.

Interestingly, this comes at a time where trucking costs are rising and as we saw in the Swift 2Q reporting, OR rates are starting to increase (SWFT 2Q2016 OR rate was 92.7% - highest in the last three years). JB Hunt sees margin erosion in the latter half of the year for both trucking and intermodal. Great if you are a shipper as soon trucking companies will start working to get any contribution to fix but bad if you are an investor or a trucking company itself.

Starting in late 2015 and through this year, the pricing index has gone down and continues to go that direction.

Starting in late 2015 and through this year, the pricing index has gone down and continues to go that direction.

Suffice to say, Intermodal is following the same trends.

So, what is going on here? Why do we continually get told that "this is the year" and yet for the last 3 years at least, the tightening has never arrived? I attribute it to three main items:

1. The Economy is not nearly as robust as you may think watching the markets. Remember, finance (which requires no trucking) has grown to be a substantial part of our economy. In the past when you said GDP went up x% you could correlate that directly to an increase in the need for transportation of goods. Today, that is untrue.

2. Inventory levels remain elevated. Think of it this way, when inventory levels are as high as they are this essentially means you shipped the product in previous quarters. This is like "borrowing" against the future. Made those quarters look good but because there was not enough sell through, the product just sat and now when sales tick up, the inventory has already been shipped.

3. Miniaturization, packaging and digitization of products. I have always said the shippers would not sit idly by and just watch rates go up. They have figured out ways to streamline packaging, digitize what they can (including the growth of 3d printing, and make things smaller. This means less transportation capacity needed.

Overall, given the way the economy is headed, I would be shocked if 2017 was anything different. Hunker down, we are in for a bit of a ride here.

For the last three months, the truckload index has decreased 2.3%, 1.2% and 1.8% respectively and the graph shows how difficult this market has become. We now are looking into 2017 before there is any tightening of capacity and pricing. I believe capacity will need to exit the market as not only is there too much today but the economy will start slowing and that means just the normal cycle would require removal of capacity. Interestingly, this comes at a time where trucking costs are rising and as we saw in the Swift 2Q reporting, OR rates are starting to increase (SWFT 2Q2016 OR rate was 92.7% - highest in the last three years). JB Hunt sees margin erosion in the latter half of the year for both trucking and intermodal. Great if you are a shipper as soon trucking companies will start working to get any contribution to fix but bad if you are an investor or a trucking company itself.

Suffice to say, Intermodal is following the same trends.

So, what is going on here? Why do we continually get told that "this is the year" and yet for the last 3 years at least, the tightening has never arrived? I attribute it to three main items:

1. The Economy is not nearly as robust as you may think watching the markets. Remember, finance (which requires no trucking) has grown to be a substantial part of our economy. In the past when you said GDP went up x% you could correlate that directly to an increase in the need for transportation of goods. Today, that is untrue.

2. Inventory levels remain elevated. Think of it this way, when inventory levels are as high as they are this essentially means you shipped the product in previous quarters. This is like "borrowing" against the future. Made those quarters look good but because there was not enough sell through, the product just sat and now when sales tick up, the inventory has already been shipped.

3. Miniaturization, packaging and digitization of products. I have always said the shippers would not sit idly by and just watch rates go up. They have figured out ways to streamline packaging, digitize what they can (including the growth of 3d printing, and make things smaller. This means less transportation capacity needed.

Overall, given the way the economy is headed, I would be shocked if 2017 was anything different. Hunker down, we are in for a bit of a ride here.

Sunday, July 31, 2016

Supplier Compliance and Social Responsibility - Look Deep Into Your Supply Chain

The Guardian has run a great piece in their paper titled "Vauxhall and BMW among Car Firms Linked to Child Labour Over Glittery Mica Paint". This article shows the results of the paper's investigation into illegal mica mines in India and the use of child labor. Not the type of headline your company wants to have. I will summarize the impact on supply chains but you should read the full article at the Guardian website. It is a bit troubling that major companies are still claiming ignorance on issues such as this.

Of course this has huge implications for supply chains. How do you get the materials you need from thousands of suppliers and still maintain control over the way the materials are extracted and handled. This is especially important when it relates to raw materials mined from the earth. So often, these materials are mined in 3d world counties with no standards on safety or child labor. The cosmetics and car industries are learning a lot right now.

If you are responsible for any type of procurement in your supply chain and you are not actively and aggressively working with all your suppliers (Walk the "tiers" all the way back to the raw material extraction) then you are putting your company's brand and reputation in grave danger. Remember, Brand Value is only made up in trust. Trust can disappear over night. When the first thing a company says to the press after a story like this comes out is "We don't discuss supplier relations with the press" (like PPG initially did), you know they have been caught off guard. Either they had no program or it was woefully inadequate and now they are scrambling to find out what the heck is going on.

Some thoughts on what you should be doing:

Of course this has huge implications for supply chains. How do you get the materials you need from thousands of suppliers and still maintain control over the way the materials are extracted and handled. This is especially important when it relates to raw materials mined from the earth. So often, these materials are mined in 3d world counties with no standards on safety or child labor. The cosmetics and car industries are learning a lot right now.

If you are responsible for any type of procurement in your supply chain and you are not actively and aggressively working with all your suppliers (Walk the "tiers" all the way back to the raw material extraction) then you are putting your company's brand and reputation in grave danger. Remember, Brand Value is only made up in trust. Trust can disappear over night. When the first thing a company says to the press after a story like this comes out is "We don't discuss supplier relations with the press" (like PPG initially did), you know they have been caught off guard. Either they had no program or it was woefully inadequate and now they are scrambling to find out what the heck is going on.

|

| Picture from The Guardian |

Some thoughts on what you should be doing:

- Prioritize Social Responsibility and Responsible Sourcing Strategies by appointing a "C" level executive as the program sponsor.

- If a price for an item or for materials is "too good to be true" then it probably is and you should investigate.

- Have a no tolerance policy. No "slaps on the wrist" but rather eradicate from your portfolio any supplier who is non compliant.

- Have "boots on the ground" in all countries where you have significant presence. If you know the "sparkle in the paint" comes from mica in India and you know it is mined - you need to be there. Someone needs to go and inspect (It always amazes me how these newspapers can find it with no problem but the key executives will say 'I had no idea.. '.

Finally, as consumers, we need to continue to ask and probe before we buy. Before you buy that sparkling new car with the beautiful metallic paint, do a little research. You may find out your beautiful car is a product of a 7 year old with a pick axe breathing toxic materials and being sentenced to a life of what is essentially slavery.

Help Adrian Gonzalez Raise $10K to Fight Type 1 Diabetes!

Anyone who has been in this industry for more than a day probably knows Adrian, has heard of Adrian or has watched his great videos on Talking Logistics. He is working for a great cause and that is to stamp out Type 1 Diabetes and he is going to do a 100 mile bike ride in Death Valley to show his commitment.

Let's all rally around him and sponsor him. You can submit your donation / sponsorship on JDRF Ride to Cure Diabetes Page. Let's support him!

Let's all rally around him and sponsor him. You can submit your donation / sponsorship on JDRF Ride to Cure Diabetes Page. Let's support him!

Monday, June 27, 2016

Macroeconomic Monday® Special Edition - Watch the Debt

I have read two major books recently on the economy - one old and one new. Both appear to be seminal books on what drives economic booms, busts and panics. The two books are: 1) The Makers and The Takers: The Rise of Finance and The Fall of American Business by Rana Foroohar. 2) Manias, Panics and Crashes: A History of Financial Crises by Robert Z. Aliber.

The theme of both books is excess debt plays a huge role in the build up to any recession (or worse, depression). The cycle goes something like this:

The graph the the left depicts the issue at hand. As you can see from this chart our overall household debt is almost at pre-recession levels. Two other key points are clear from this chart:

The graph the the left depicts the issue at hand. As you can see from this chart our overall household debt is almost at pre-recession levels. Two other key points are clear from this chart:

This graph shows more detail on the auto sub-prime loans (When you see your friend get that new BMW, you have to wonder where the money came from). You can see that auto sub-prime really telegraphed the previous recession and then people clamped down on their borrowing to right their personal balance sheets.

This graph shows more detail on the auto sub-prime loans (When you see your friend get that new BMW, you have to wonder where the money came from). You can see that auto sub-prime really telegraphed the previous recession and then people clamped down on their borrowing to right their personal balance sheets.

The theme of both books is excess debt plays a huge role in the build up to any recession (or worse, depression). The cycle goes something like this:

- Recovery begins through stimulus or some other external event (think war spending).

- The cycle takes off and should become self sustaining (Although we never saw that this cycle)

- Eventually it starts losing steam. In order to keep it going, we need to incur higher and higher amounts of debt.

- In order to keep the higher debt going, we have to allow sub-prime to participate. Not only does debt go up but debt quality goes down.

- Eventually, defaults begin.

- People begin hoarding cash and spending less as they fear the economic downturn. This causes more defaults as layoffs begin. The downward spiral begins.

- Voila! Recession or worse and then we start all over again.

This has been the case for hundreds of years (despite people wanting to go back to the "good old days", hard depressions are less harsh now and certainly less frequent). As we see freight volumes going down and with that, freight rates going down, I have to ask, are we starting to see this cycle in its later stages? Certainly, we are at the tail end of an expansion but what does the debt data tell us?

In this and subsequent editions of Macroeconomic Monday® I am going to attempt to explain where I think we are. Today, we will look at three topics: The overall debt (Household) in the nation, the makeup of that debt and finally the quality of auto loans.

The graph the the left depicts the issue at hand. As you can see from this chart our overall household debt is almost at pre-recession levels. Two other key points are clear from this chart:

The graph the the left depicts the issue at hand. As you can see from this chart our overall household debt is almost at pre-recession levels. Two other key points are clear from this chart:- The debt level relative to 2003 is incredibly high.

- The amount of debt due to student loans has grown exponentially (yes, this is a big problem - student loans cannot be discharged in bankruptcy and do not have physical assets behind them).

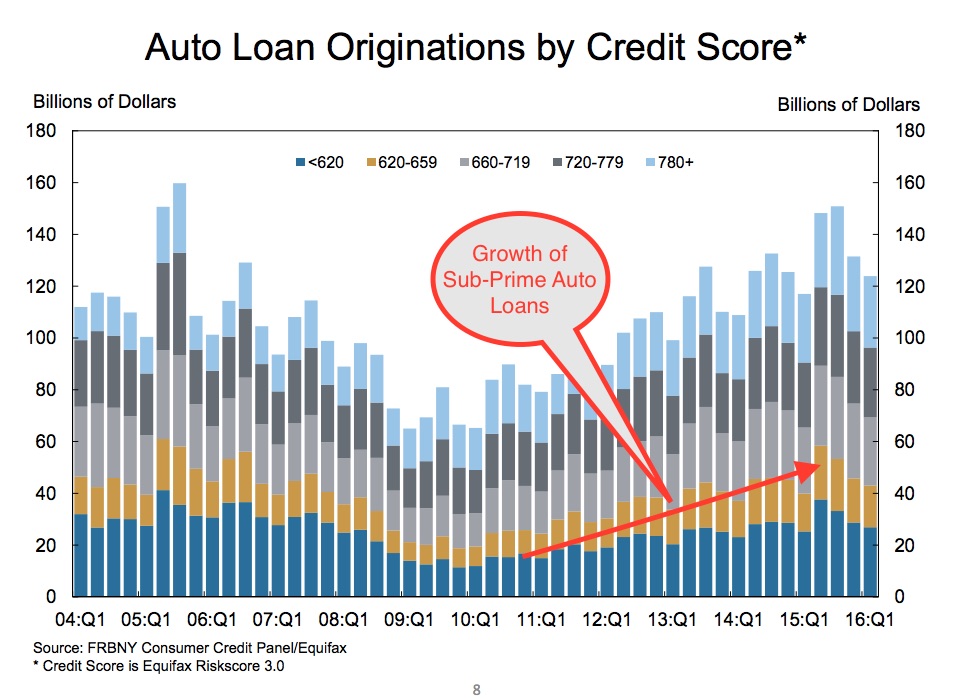

Mortgage debt is still inflated and the very interesting part of this chart is the growth of auto loans. The key part to this, as explained in the graph below, is more and more auto loans are made to the sub-prime sector of the economy.

This graph shows more detail on the auto sub-prime loans (When you see your friend get that new BMW, you have to wonder where the money came from). You can see that auto sub-prime really telegraphed the previous recession and then people clamped down on their borrowing to right their personal balance sheets.

This graph shows more detail on the auto sub-prime loans (When you see your friend get that new BMW, you have to wonder where the money came from). You can see that auto sub-prime really telegraphed the previous recession and then people clamped down on their borrowing to right their personal balance sheets.

However, really since about 2011 this has changed and the sub-prime borrowing started taking off again. This was almost fully due to automobile companies needing to keep the "post recession party" going.

So, our first lesson is pretty clear, and stark. Personal debt is growing and total debt is almost at the pre-recession levels. For one of the biggest and riskiest categories (auto loans), sub-prime debt is increasing. Finally, student debt, which stops or delays household formation, is clearly at unsustainable levels.

Following our guidance in the two books I mentioned above, this is the "brake" on the economy which never lets the flywheel turn on its own. It is also why markets go into turmoil every time Janet Yellen even remotely mentions increasing interest rates. This brake is why freight volumes are down, we have over capacity in transportation and rates are starting to plummet. If people do not buy, companies do not make and therefore freight capacity exceeds volumes and rates go down. It is that simple.

So, the next time someone says to you "things will get better next year", remember the debt story. They cannot get better when more and more money is going to pay interest on debt incurred for items already purchased. And, of course, this is why you are seeing negative interest rates as central banks realize that is the only way to fight this. But, more on that next time.

Sunday, June 26, 2016

Revisit "Favored Shipper" During Downturn in Rates

I have advocated over and over that the idea of getting better rates because you are a "favored" or "preferred" shipper is a red herring. The idea that a trucking company will take less in profit because you are preferred just does not make sense.

In the environment of rate reductions and over capacity I am sure shippers are starting to hear the same old mantra from the trucking companies: "Stick with us and pay higher than market rates. Once the "worm turns" we will stick with you". This is the logic. Yet by all accounts, even the transportation executives believe transportation is a commodity play. Less capacity and more demand = prices go up. More capacity and less demand = prices go down. That simple.

I had been somewhat a lonesome person in this argument until C.H. Robinson, along with Iowa State University, attempted to quantify this with a white paper entitled: Do "Favored Shippers" Really Receive Better Pricing and Service. Let me cut to the chase and let you know the answer is NO. Here is a quote:

So, remember, no matter what you do in terms of "market rates" what really matters is dwell time. The research clearly suggests that regardless of what you do in terms of rates now, in the future, it is all about dwell time and if you do not have best dwell time, what you did when rates turned down will be meaning less.

My advice is the same now (and even strengthened) as it always has been. Take what is yours in terms of rates because the trucking company will take what is theirs when the environment changes. Then, of course, do the right thing and keep the trucks moving.

In the environment of rate reductions and over capacity I am sure shippers are starting to hear the same old mantra from the trucking companies: "Stick with us and pay higher than market rates. Once the "worm turns" we will stick with you". This is the logic. Yet by all accounts, even the transportation executives believe transportation is a commodity play. Less capacity and more demand = prices go up. More capacity and less demand = prices go down. That simple.

I had been somewhat a lonesome person in this argument until C.H. Robinson, along with Iowa State University, attempted to quantify this with a white paper entitled: Do "Favored Shippers" Really Receive Better Pricing and Service. Let me cut to the chase and let you know the answer is NO. Here is a quote:

"Carriers cite many attributes that may result in "shipper of choice" status. Research shows that keeping the driver moving and generating income is more important to these carriers than keeping a shipper as a customer".The bottom line is that dwell time of the driver is the overriding factor to determine if you will get best price or not. And really, it is not even the driver rather it is the trucking company asset (Truck and trailer) they truly care about.

So, remember, no matter what you do in terms of "market rates" what really matters is dwell time. The research clearly suggests that regardless of what you do in terms of rates now, in the future, it is all about dwell time and if you do not have best dwell time, what you did when rates turned down will be meaning less.

My advice is the same now (and even strengthened) as it always has been. Take what is yours in terms of rates because the trucking company will take what is theirs when the environment changes. Then, of course, do the right thing and keep the trucks moving.

Subscribe to:

Posts (Atom)