I have read two major books recently on the economy - one old and one new. Both appear to be seminal books on what drives economic booms, busts and panics. The two books are: 1) The Makers and The Takers: The Rise of Finance and The Fall of American Business by Rana Foroohar. 2) Manias, Panics and Crashes: A History of Financial Crises by Robert Z. Aliber.

The theme of both books is excess debt plays a huge role in the build up to any recession (or worse, depression). The cycle goes something like this:

- Recovery begins through stimulus or some other external event (think war spending).

- The cycle takes off and should become self sustaining (Although we never saw that this cycle)

- Eventually it starts losing steam. In order to keep it going, we need to incur higher and higher amounts of debt.

- In order to keep the higher debt going, we have to allow sub-prime to participate. Not only does debt go up but debt quality goes down.

- Eventually, defaults begin.

- People begin hoarding cash and spending less as they fear the economic downturn. This causes more defaults as layoffs begin. The downward spiral begins.

- Voila! Recession or worse and then we start all over again.

This has been the case for hundreds of years (despite people wanting to go back to the "good old days", hard depressions are less harsh now and certainly less frequent). As we see freight volumes going down and with that, freight rates going down, I have to ask, are we starting to see this cycle in its later stages? Certainly, we are at the tail end of an expansion but what does the debt data tell us?

In this and subsequent editions of Macroeconomic Monday® I am going to attempt to explain where I think we are. Today, we will look at three topics: The overall debt (Household) in the nation, the makeup of that debt and finally the quality of auto loans.

The graph the the left depicts the issue at hand. As you can see from this chart our overall household debt is almost at pre-recession levels. Two other key points are clear from this chart:

- The debt level relative to 2003 is incredibly high.

- The amount of debt due to student loans has grown exponentially (yes, this is a big problem - student loans cannot be discharged in bankruptcy and do not have physical assets behind them).

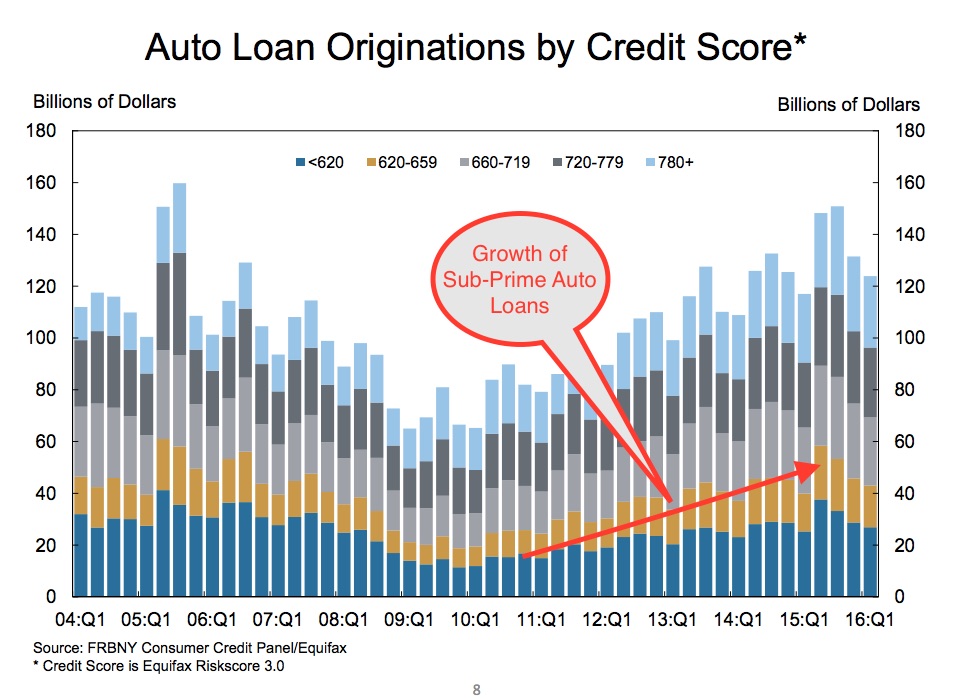

Mortgage debt is still inflated and the very interesting part of this chart is the growth of auto loans. The key part to this, as explained in the graph below, is more and more auto loans are made to the sub-prime sector of the economy.

This graph shows more detail on the auto sub-prime loans (When you see your friend get that new BMW, you have to wonder where the money came from). You can see that auto sub-prime really telegraphed the previous recession and then people clamped down on their borrowing to right their personal balance sheets.

However, really since about 2011 this has changed and the sub-prime borrowing started taking off again. This was almost fully due to automobile companies needing to keep the "post recession party" going.

So, our first lesson is pretty clear, and stark. Personal debt is growing and total debt is almost at the pre-recession levels. For one of the biggest and riskiest categories (auto loans), sub-prime debt is increasing. Finally, student debt, which stops or delays household formation, is clearly at unsustainable levels.

Following our guidance in the two books I mentioned above, this is the "brake" on the economy which never lets the flywheel turn on its own. It is also why markets go into turmoil every time Janet Yellen even remotely mentions increasing interest rates. This brake is why freight volumes are down, we have over capacity in transportation and rates are starting to plummet. If people do not buy, companies do not make and therefore freight capacity exceeds volumes and rates go down. It is that simple.

So, the next time someone says to you "things will get better next year", remember the debt story. They cannot get better when more and more money is going to pay interest on debt incurred for items already purchased. And, of course, this is why you are seeing negative interest rates as central banks realize that is the only way to fight this. But, more on that next time.