The scorecard: Dow up 307.41 points and up 9.87% for the year.

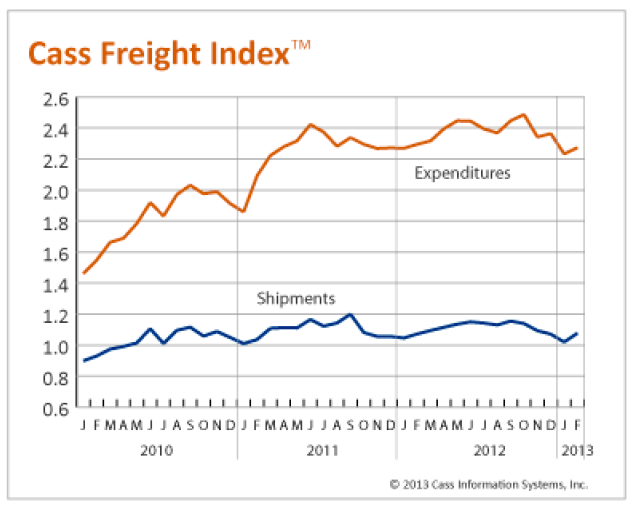

As always however I like to look at things through the eyes of logistics. What does this mean for logistics (i.e., freight movement and storage) in this country? When I look at it through that lens I see a lot of other data which continues to support the idea that the production and movement of goods is still very lackluster. Let's look at a few:

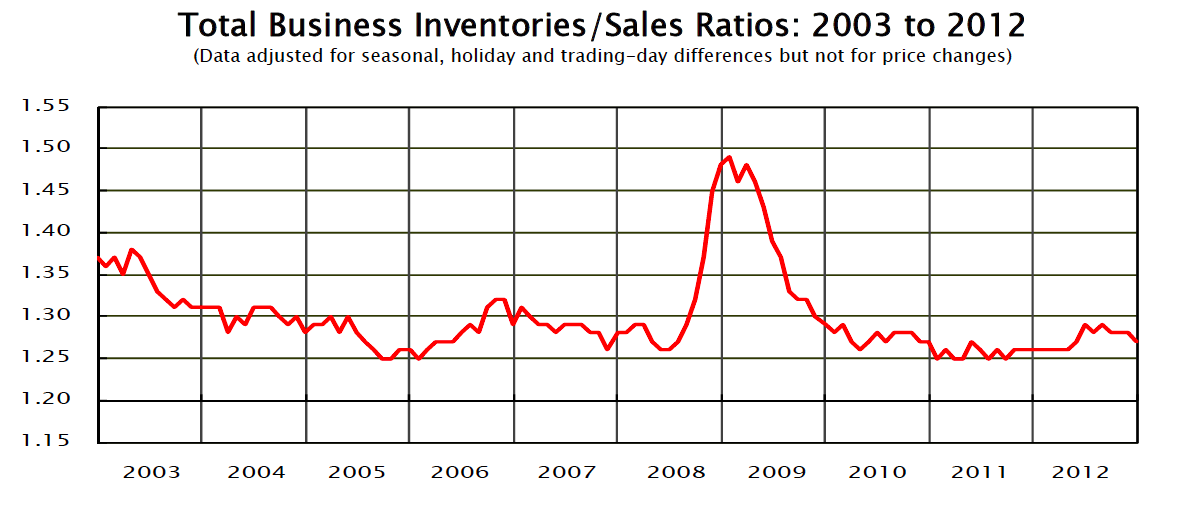

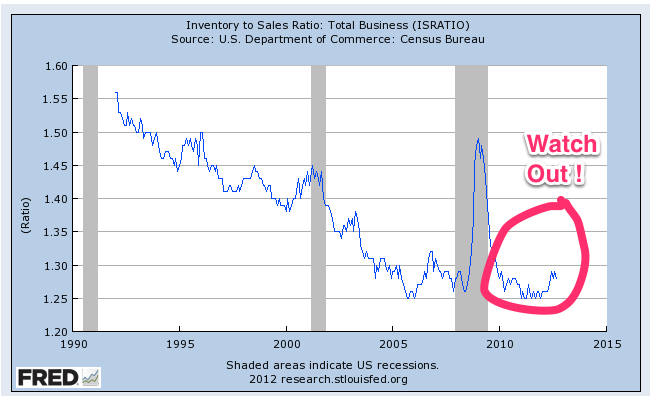

Monthly Wholesale Inventories Relative to Sales:

This number (Unlike the Total number reported on earlier) climbed 1.2% which tells us that inventory is beginning to back up at the wholesale level and will ultimately either need to be sold or production will have to slow down. Most of this increase is in the durables number and represents an increase from a revised December number and a significant increase over January 2012. Interesting that sales of durables are up however the inventory has grown faster than sales.

McDonald's Same Store Sales were Down: Of course the company blames this on the lack of the extra leap day and that could be true but, I generally dismiss these types of excuses. At the end of the day if they are that close then they are flat at best. I use McDonalds as a barometer for world spending because it is just about everywhere and almost everyone goes there. If you are out shopping, you probably will stop at a McDonalds sometime so it is a good measuring stick. I know, not very scientific but these types of indicators generally work.

Personal Income and Outlays: This was down 3.6% in January (released March 1) which again is an early indicator of not much activity in the economy which will be good.

Countering this type of news was the great news on the unemployment rate going down to 7.7%. This is fantastic however I report it with one caution and that caution deals with the sequestration. Most government agencies will be dealing with budget cuts via furloughs and not lay offs. This means while the unemployment number may appear relatively unscathed during this time people's spending will decrease as they have less disposable income and are less secure.

Of course, these statistics reported in March for January are all at least 1 month old and it is theoretically possible the market is acting as a leading indicator on the physical economy rather than the financial economy. But I doubt it.

While my meter is up and I am hoping this is the beginning of a massive boom in the physical economy I think the data says this is a financial economy activity. Companies, while selling the same or less, are making a lot more money, have a lot of cash and the alternative investment, treasuries, barely keep up with inflation. For these reasons I believe the market is skyrocketing and may well continue.

The question is will it translate into physical goods. Right now the data says... Maybe.... .(OK, my meter may have moved just a bit to the right from absolutely no to .. Maybe)