NPR does a very good podcast on the "math behind the packages". A very fascinating quick story on how the "quants" are taking over logistics as well as finance. Being able to develop mathematical algorithms is critical to UPS' mapping success. Their mapping success is critical to the efficient routing of drivers.

Have a listen and enjoy:

A 25 year veteran of the supply chain and logistics industry blogs on all things logistics. Experience in 3PL, automotive and consumer goods logistics help bring a unique insight to this topic

Tuesday, December 18, 2012

Lessons From Kozmo.com for Same Day Delivery

Yes, it is true if you live long enough what is old will be new again. This, of course, is the situation as it relates to the so called same day delivery wars. I have mentioned over and over again that I am very skeptical of this beyond being a marketing hype ploy as the density needed (low miles per stop and high number of packages per stop) is virtually unachievable except in very dense cities. And, of course, in those cities "couriers" have been around a long time so same day delivery is not new.

Now even our friends at the Wharton School of Business have weighed in on this by analyzing what went wrong in the late '90s with Kozmo in a posting entitled " Same Day Delivery: This Time it May Actually Work" - an organization dedicated to same day delivery which went out in a flash of glory - and why this time it may be different. The basis of this argument? It is all about density.

The issues remain and the questions continue to go unanswered in my humble opinion. Some of them are:

Now even our friends at the Wharton School of Business have weighed in on this by analyzing what went wrong in the late '90s with Kozmo in a posting entitled " Same Day Delivery: This Time it May Actually Work" - an organization dedicated to same day delivery which went out in a flash of glory - and why this time it may be different. The basis of this argument? It is all about density.

The issues remain and the questions continue to go unanswered in my humble opinion. Some of them are:

- How will you get the density?

- How will you overcome the high costs of fuel?

- Will this really generate incremental sales?

- What happens when this becomes "an expectation"?

- Will this be given away for free and ultimately put pressure on margins?

- Do people even want it (beyond the procrastinators who are probably not your best customers)?

The answer to number 6 equates to the idea of sticking a knife in a horse to get one last gallop out of it before you run it to death (i.e., What Kris Kristofferson does in True Grit). Every retailer is fighting over that last incremental dollar as if it will make or break them. My analysis suggests the amount of money spent to get that very last dollar of revenue probably is not worth it however that is what they are doing as a crowd. They want that last dollar and appear to be ready to spend a fortune to get it.

In my next posting on Same Day Delivery, I will propose a solution to this issue and we shall see what they think.

Monday, December 17, 2012

IDC 2013 Supply Chain Predictions

Last night I sat through the archived broadcast of the 2013 supply chain predictions for manufacturers from IDC. While it is a little bit of "mom, Country and apple pie" I do think it was a very good presentation as it summarized almost all the key supply chain challenges in one spot. I would not say this was a "2013" prediction but rather a good primer on what supply chains always have to deal with and what should be in your playbook. Some years one will be prioritized over another (for example they believe responsiveness and service will override cost in the year ahead) but overall these are the items you are always reviewing as you develop both tactical and strategic plans.

Here are the top 10 as they see it:

Here are the top 10 as they see it:

- Resiliency becomes a priority for end users looking to master massive multidimensionality.

- Prioritize flexibility, visibility and agility

- Mastering this will require you to deal with massive amounts of data.

- On the supply side of your supply chain, recognizing inherent cost of long lead times, end users will look at global networks through the lens of both regional and country level sourcing.

- Finally companies will quantify the effect of long lead times.

- Trade offs will be made - Most effective sourcing will take over from "low cost" sourcing as companies build tools to quantify the true costs of these activities [ this bullet is my commentary].

- On the demand side of supply chain, recognizing the need for better service levels and mass customization, end users look again to postponement techniques and data analytics to drive more effective customer insights and smarter fulfillment.

- End user IT organizations must support a more productive supply chain ecosystem.

- Service excellence becomes a strategic priority.

- Supply chains optimize omnichannel customer service and cost by enabling trustworthy, efficient and effective supply chains (TEE).

- The consumer will demand value and trustworthiness (right product, right time, right place, right value).

- End user supply chains focus efforts to improve collaboration both upstream with suppliers and downstream with customers to better compete in a faster world.

- Sales and operations planning (S&OP) collaboration will be critical [ my commentary]

- Technology to bind business partners together and to facilitate the flow of information [ my commentary] will also be critical.

- The modern supply chain gets smarter

- Integration

- Optimization

- Embedded analytics

- Supply chains invest in technologies that enable visibility, virtualization, and visualization

- The 'Big Data' era draws dawns for supply chain organizations (what prediction would be complete without mentioning "big data" - my comment)

Those are the 10 and most will say this is what I do all the time as we always are trying to figure out the perfect mix of all of these things. I would agree. However, it was very helpful to get it all in one spot and perhaps use a maturity model to rate your supply chain - where are you on each of these dimensions and how important is that dimension to your organization.

Once you draw that out graphically you can then socialize it in your company and begin drawing out what your 3 - 5 year strategy will look like along with what tactics you may use next year.

Sunday, December 16, 2012

Do You Have a Supply Chain or a Spiderweb?

This question was recently asked by Zurich's "Risk Engineers" and I think it is a fascinating question. The metaphor we are all familiar with, the "supply chain" connotes a nice set of interlocking rings, probably made of steel, and that are perfectly aligned. It brings to mind a very planned and organized way to get from point "a" (raw materials) to point "b" (finished goods) to point "z" (The consumer). We all know the problems recently experienced from hurricane Sandy however this study clearly indicates the issue is deeper and more broader than just a freak storm.

Reality is, unfortunately, many are spiderwebs. Not made in any particular order, overlapping and easily disrupted with the swat of a hand. Zurich believes 2013 is the year companies better take managing, or at least mapping, this web a bit more seriously. A few key statistics:

Reality is, unfortunately, many are spiderwebs. Not made in any particular order, overlapping and easily disrupted with the swat of a hand. Zurich believes 2013 is the year companies better take managing, or at least mapping, this web a bit more seriously. A few key statistics:

- 73% of respondents to a survey in 2011 reported at least one supply disruption; 50% reported two.

- 40% of those who experience extended disruptions eventually go out of business.

- The leading cause of disruptions is IT or telecommunications. 52% saw some or a high level of disruption from these issues.

- One in five companies said they had one instance where they incurred at least $161M in damages

I had an opportunity many years ago to meet with the people of Zurich about this topic in New York City. At that time it was an "interesting"topic but not much more. Today, it is critical. Terrorism, global warming, reliance on sophisticated telecommunications networks, "just in time" (i.e., lack of buffer stocks) and the web of globalization has not only made the likelihood of a disruption more probable but the consequences of it far more severe.

Their solution is at least to start mapping out your supply chain through tier 2 and rate it based on likelihood of disruption, financial stability and physical stability. From there I imagine you can create significant contingency plans to at least have a fighting chance at keeping your business running.

Saturday, December 15, 2012

Wednesday, December 12, 2012

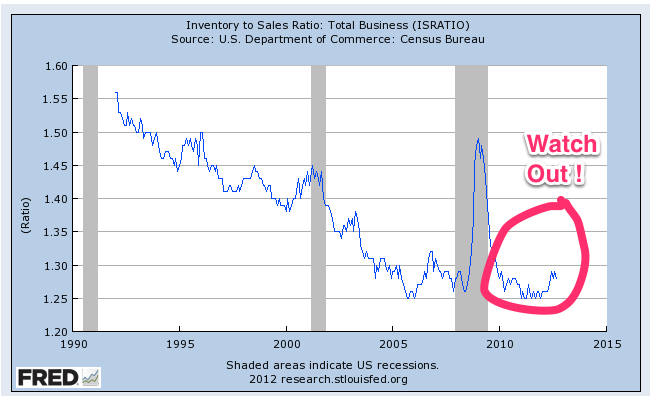

Inventory to Sales Ratio Tells a Grim Story

As my readers know I follow this very closely as this ratio tells us whether product is "backing up" in the supply chain or flowing as it should from manufacturer to consumer. We are already hearing anecdotes of sales not being where they should be for the holidays, slow movements of imports, extended automotive shutdowns and now this... the inventories in the pipeline relative to sales are growing:

|

| Inventory to Sales - Published 12/11/2012

The slope of the line looks very ominous and it certainly looks like it did back in the 2006 time frame. Of course, we came out of that but only for a short period before we had a collapse. This clearly leads us to believe freight will be very soft for Q1 and perhaps into Q2 as companies execute the "final mile" by selling what is inventory but not restocking until these inventories get back to normal.

Some may look back into the '90's and say "we have a long way to go before we get to those levels". To this I say retailers and manufacturers learned their lesson during the "great recession" and I would not anticipate ever going back to those levels of inventory (At least until those who lived through the great recession die off then the new younger hip crowd says "this time is different" and go back to it - it is a generational cycle).

This data, along with the idea that we will have extended automotive shutdowns (at least with GM on the Cruze line) leads me to believe my prediction for soft freight in the first half of the year is very reasonable.

As always, I hope I am wrong however I truly just let the data speak.

|

Friday, December 7, 2012

Where Reverse Logistics and Sustainability Meet

We all know the technical reasons for reverse logistics and at this point in the season many retailers loathe it. Product is returned, packaging is just thrown into landfills and old product is thrown in the garbage in favor of the new and fancier version. This is both a reverse logistics and a sustainability nightmare.

What is worse is a lot of the garbage created ends up in the ocean. There are floating patches of man made waste all over the ocean and it just sits out there generally making a mess of things.

Well, fret no more as one of the most forward thinking and sustainable companies on the planet, Method, has come to the rescue. According to both their website and this article in the Mother Nature Network Method has devised a way to take that post consumer use ocean garbage and re-purpose it to make the bottles for their 2 in 1 hand soap / dish wash soap. What a great idea. by using this product you will accomplish three things:

What are you doing for your personal sustainability initiative today?

What is worse is a lot of the garbage created ends up in the ocean. There are floating patches of man made waste all over the ocean and it just sits out there generally making a mess of things.

Well, fret no more as one of the most forward thinking and sustainable companies on the planet, Method, has come to the rescue. According to both their website and this article in the Mother Nature Network Method has devised a way to take that post consumer use ocean garbage and re-purpose it to make the bottles for their 2 in 1 hand soap / dish wash soap. What a great idea. by using this product you will accomplish three things:

- Get a great soap (Yes, I use Method and love it)

- Help to clean the oceans

- Eliminate waste in the creation of new plastic bottles which are unneeded since we as humans have provided patches of the old stuff ready for use.

It is very rare you can accomplish all of this in one purchase. Yes, recycling what we throw away is part of reverse logistics.

What are you doing for your personal sustainability initiative today?

Exporting Natural Gas - No Cheap gas Part deux

I wrote back in the beginning of November that we can expect an abundance of domestic oil and gas but not low price oil and gas. I said this because what the candidates refused to say was that while it is abundant the fact it all can be exported means it will almost always stay around the world price for oil and gas. My thesis was if the price in the US just became too cheap all of it would be exported.

I hate it when the facts prove this out.

Today in the Wall Street Journal there is an article titled "US Gas Exports Clear Hurdle" and it is talking about a Government study which said was good for the economy if we "liquefied and exported" natural gas. Voila.. your "cheap domestic source of energy" has just evaporated into a world price domestic source of energy. So, those expecting a great amount of domestic energy and all the good things that come with this should be happy.

Those who expected "cheap" energy will be disappointed.

I hate it when the facts prove this out.

Today in the Wall Street Journal there is an article titled "US Gas Exports Clear Hurdle" and it is talking about a Government study which said was good for the economy if we "liquefied and exported" natural gas. Voila.. your "cheap domestic source of energy" has just evaporated into a world price domestic source of energy. So, those expecting a great amount of domestic energy and all the good things that come with this should be happy.

Those who expected "cheap" energy will be disappointed.

Monday, November 19, 2012

McDonalds - No Product Out of Stock - Ever!

I like it when a company knows and understands its core principles relative to the supply chain. I see so many companies make the mistake of trying to develop a culture where everyone can suggest trade-offs. When that happens then everyone has a great idea on what should come first, second and third in terms of priority.

In this article titled, McDonalds Wants to Be Assured of Delivery, the McDonalds Director of Global Supply Chain Integration and Logistics, Alex Bahr makes it pretty clear that first and foremost nothing can be out of stock - ever. And, it is for a very simple reason: efficiency of the restaurants. He states:

Clarity brings simplicity and unity of purpose for a team. Are your supply chain objectives this clear?

In this article titled, McDonalds Wants to Be Assured of Delivery, the McDonalds Director of Global Supply Chain Integration and Logistics, Alex Bahr makes it pretty clear that first and foremost nothing can be out of stock - ever. And, it is for a very simple reason: efficiency of the restaurants. He states:

"A typical McDrive needs to be able to handle 120 cars per hour in Europe, and as many as 150 to 160 cars per hour in the US. That leaves us no time to suggest alternatives if a product is out of stock."I believe more supply chains need to be just this blunt on what the priorities are. I once worked in automotive service parts where the objective was 80% of last nights orders are delivered by 10:00am the next day and the remaining 20% were delivered by the end of the day. This was a "non-negotiable" standard and any cost cutting project had to be done in the context of this objective. An idea which said we could save $xx dollars if we pushed delivery out a day was rejected immediately.

Clarity brings simplicity and unity of purpose for a team. Are your supply chain objectives this clear?

Sunday, November 18, 2012

Discussion at Michigan State

I had the pleasure of speaking to the Broad China Business Society this past Friday concerning my thoughts on where global logistics is headed, what are the big issues or mega-trends and what are some of the things we logisticians can do to solve these issues. I first want to thank the group for inviting me and say how incredibly impressed I was with the leadership and the membership of this group. All incredibly intelligent students and it makes me feel really positive about our future. With these students as leaders, the world is in good hands.

After showing the state of our industry as measured by efficiency and quantity of goods (the state is healthy but has some challenges) I then went into 5 major challenges:

After showing the state of our industry as measured by efficiency and quantity of goods (the state is healthy but has some challenges) I then went into 5 major challenges:

- The continued rapid explosion of global trade

- The evolving infrastructure issues around the world

- Global security issues - this deals with supply chain disruption for any reason

- Global climate and sustainability issues

- The "war" for talent and the need for great talent in our industry.

While I will not go into this in depth here I do believe all of these issues are issues the logistician and the supply chain professional will need to study and deal with over the next 10 - 20 years. Each person will have to evaluate these areas relative to the industry they are in, the goals and objectives of their business and their business' current situation.

I warn people - there are not one size fits all solutions to these issues. What works for a CPG company may not work in consumer durables. Again, the tough work of detailed analysis in your own business must be done to determine where you will take your strategy.

I also caution people to reevaluate these periodically. While these trends will stay with us the severity of each one may change which may change your prioritization of what to work on.

The discussion was almost an hour long so the details are beyond the scope of a blog. Thank you again to Michigan State University and I hope to do this again soon!

Is The Apple Supply Chain in Trouble?

Forbes is questioning the efficiency of the Apple supply chain now that Tim Cook is running the company and not just the supply chain and operations. I think this is a bit of a stretch and also a bit of hype as everyone tries to find issues with the leader. I doubt very much if anything substantively has improved or devolved since Tim Cook took over the entire company - things don't "rust" that fast.

The future will tell however I would hate to be part of the millions of people who have counted Apple down for the count more than once. It is a great company and will be for quite some time.

The future will tell however I would hate to be part of the millions of people who have counted Apple down for the count more than once. It is a great company and will be for quite some time.

Thursday, November 15, 2012

Cap and Trade Has Come To Be in California

Consider it a birthday of sorts. Yesterday, California launched their first "Cap and Trade" market by auctioning off allowances in the California Carbon market. This, while just being California, actually becomes the world's second largest carbon market right behind all of the European Union.

While right now it essentially only applies to major refineries and electric plants the day is coming when it will apply to transportation fuels. My personal recommendation is the industry should get prepared to deal with this inevitability rather than fight it. Politics aside, what we have found is what generally starts with the California Air Resource Board (CARB) moves across the Nation fairly quickly.

The Wall Street Journal reports on this launching and reports California expects to raise $1bl in 2012 and $2.8 to $11bl by 2015. A critical factor for success is we have to ensure this money goes to actually reducing emissions or offset projects rather than the general coffers of the state. If we can avoid the "money grab" then this will be a very effective way to use market incentives to lower emissions.

According the the California auction site, the results will be listed on November 19, 2012. Auction information can be found at the CARB auction site.

While right now it essentially only applies to major refineries and electric plants the day is coming when it will apply to transportation fuels. My personal recommendation is the industry should get prepared to deal with this inevitability rather than fight it. Politics aside, what we have found is what generally starts with the California Air Resource Board (CARB) moves across the Nation fairly quickly.

The Wall Street Journal reports on this launching and reports California expects to raise $1bl in 2012 and $2.8 to $11bl by 2015. A critical factor for success is we have to ensure this money goes to actually reducing emissions or offset projects rather than the general coffers of the state. If we can avoid the "money grab" then this will be a very effective way to use market incentives to lower emissions.

According the the California auction site, the results will be listed on November 19, 2012. Auction information can be found at the CARB auction site.

Wednesday, November 14, 2012

Speaking at Michigan State

If any readers are near Michigan State this Friday, I am keynoting at the Broad China Supply Chain Forum. My topic will be on The Current and Future State of Global Logistics. I will also be on a panel concerning sustainability.

Stop by and say hi!

Stop by and say hi!

Tuesday, November 13, 2012

Oil Independence? Yes - "Cheap" Oil? - No

I have written about this before because I feel the headlines are misleading for those in energy intensive industries such as transportation. The headlines talk about energy independence and energy dominance and the underlying assumption by most is this will translate into low cost oil. This could not be further from the case.

We will continue to have high priced oil and the IEA in the same report where they said the US will be the dominant producer of oil also said you can expect oil priced at $125 per barrel (inflation Adjusted). Oil is a global commodity and therefore will settle on global prices. The Wall Street Journal in an article entitled "Don't Expect Lower Oil Prices Even As US Output Surges" quotes the report by saying:

We will continue to have high priced oil and the IEA in the same report where they said the US will be the dominant producer of oil also said you can expect oil priced at $125 per barrel (inflation Adjusted). Oil is a global commodity and therefore will settle on global prices. The Wall Street Journal in an article entitled "Don't Expect Lower Oil Prices Even As US Output Surges" quotes the report by saying:

"But oil prices, the IEA said, will continue to rise, hitting $125 per barrel in inflation-adjusted terms — more than $215 per barrel in nominal terms — by 2035. U.S. consumers, the agency makes clear, won’t be shielded from those price increases, even if the country doesn’t import a drop of foreign oil."The report goes on to say:

"Oil is a global commodity. What matters for prices is total supply and total demand — not where the oil is produced or consumed. That means that even if the U.S. relied only on domestically produced oil, prices would still be dictated by global market forces."Oil prices are based on global supply and demand and oil is very easily exported. As soon as there is a big enough price differential where traders can make money in arbitrage they will export the oil. The graph below shows the predictions by the IEA:

So, the conclusion is clear... The US will be a large oil producer AND you will still be paying $3.00 - $4.00 in adjusted dollars per gallon.

Monday, November 12, 2012

An Interesting Post On Value of Supply Chain MBA

20 years ago "plus" when I started in this industry I would not have even been able to tell you where to get a "supply chain MBA". Usually it was finance or operations research degrees who somehow meandered into this field.

This is not true anymore and this blog post from "The Strategic Sourceror" explains why.

This is not true anymore and this blog post from "The Strategic Sourceror" explains why.

EU Freezes Carbon Charge on Airlines

Many know the EU was going to charge a carbon emissions charge on any airline flying in the EU airspace - this included foreign airlines. Of course, this caused a furor in international relations and the US actually passed legislation (prior to the election) preventing US flagged air carriers from implementing this charge.

Now, the EU has agreed to "freeze" this for a year. This is an interesting development and one which I am sure is designed to bring "peace". I am just not sure what they are waiting on? What will really be different next year than this year?

Now, the EU has agreed to "freeze" this for a year. This is an interesting development and one which I am sure is designed to bring "peace". I am just not sure what they are waiting on? What will really be different next year than this year?

Bill Graves on Fox Business

Bill Graves, the head of the American Trucking Association (ATA) does a nice job on Fox Business discussing the impact of Sandy, the readiness of the transport industry and the future of the industry.

I found it fascinating that he believes we will "slog along" until Q3 of 2013. I think this was about as direct as I have heard an industry leader speak about the "flat lining" of the transportation industry recently.

I found it fascinating that he believes we will "slog along" until Q3 of 2013. I think this was about as direct as I have heard an industry leader speak about the "flat lining" of the transportation industry recently.

U.S. Overtakes Saudi Arabia in Oil Production by 2030 - IEA

This is a fascinating statement and it shows how disruptive technology (i.e, the ability to extract tight oil and shale oil / gas) will really turn the world energy markets on their head. The International Energy Agency (IEA) has two reports out. The first (as reported by Bloomberg) describes how the US will overtake Saudi Arabia in oil production. Some interesting statistics:

- Last Month Saudi Arabia pumped 9.8 million barrels per day; The US 6.7 million - very close.

- US production this year will be highest since 1991.

- 83% of the US domestic oil needs were met with domestic oil supplies in the first 6 months of 2012.

The second report (again as reported by Bloomberg) tells us by 2030 natural gas will be the predominant source of energy in the United States as it will be plentiful and cheap. Both of these are incredible developments given just a few years ago people were talking about "Peak Oil".

I will add a bit of commentary on sustainable practices. I hope we as a country are wise enough to see these developments as incredible luck which gives us time to move to a more sustainable way to power our economy. If we use this as a way to get "cheap energy": which then makes the business case for sustainable energy not economically viable then we will have squandered a huge opportunity.

Also, as I have stated before, do not confuse "energy independence" with "cheap oil". The oil prices will almost always be at world levels because if they are not then the energy will simply be exported rather than consumed in the US.

The impact on transportation will be clear:

- Oil supplies abundant

- Oil prices at world levels (i.e., no "cheap oil")

- Movement to natural gas will continue.

A Good After Action Review (AAR) for Logistics Companies Post Sandy

A neat article in Reuters today titled "Transport, Logistics Weather Sandy Well Despite Glitches" calls out the great work the trucking and logistics industry is doing in Sandy. Specifically, the good news is the industry learned from Katrina and has developed very good playbooks to deal with big storms and natural disasters:

On Veterans day, we thank all the veterans who have served this Nation. I would also say if companies are preparing to work in disaster stricken areas there is no better person to lead these efforts than a veteran.

"Freight transportation company triage playbooks have been evolving with a series of disasters, including Hurricane Katrina.

By the time Sandy hit, trucking and logistics companies had topped off gas tanks, bought or rented back-up generators to power distribution and fueling centers, and shipped relief and manufacturing supplies to the Northeast that customers would need after the storm. During the storm and in the days after, these companies and East Coast railroads diverted shipments away from the hardest-hit areas and found alternative delivery options for customers"This is good news as we know these disasters will not only increase with frequency but also with severity and the fact the industry is preparing for them is a great service to the US.

On Veterans day, we thank all the veterans who have served this Nation. I would also say if companies are preparing to work in disaster stricken areas there is no better person to lead these efforts than a veteran.

Saturday, November 10, 2012

Rail Volume for Week 44 Down - Hurricane Sandy

Association of American Railroads released week 44 on Thursday and as expected volumes were down significantly. However, anyone who graphs and analyzes this data closely will need to asterisk this week forever as Hurricane Sandy drove most of it.

The data shows a 4.8% decrease in container traffic versus week 44 of 2011. This can only be explained by the Hurricane and embargo of certain locations. Container traffic through week 44 increased 5.6% for the year showing the increased volumes will continue and, as expected, trailer traffic on the rails continues its decline in favor of the more efficient COFC.

Overall ton miles are down both for the week and for the year and the driving factor for this is Coal. Coal is down substantially and while petroleum products are up due to all the shale oil it is not enough, on a ton mile basis, to offset the decrease in coal.

The story continues to unfold despite the blip due to Sandy:

The data shows a 4.8% decrease in container traffic versus week 44 of 2011. This can only be explained by the Hurricane and embargo of certain locations. Container traffic through week 44 increased 5.6% for the year showing the increased volumes will continue and, as expected, trailer traffic on the rails continues its decline in favor of the more efficient COFC.

Overall ton miles are down both for the week and for the year and the driving factor for this is Coal. Coal is down substantially and while petroleum products are up due to all the shale oil it is not enough, on a ton mile basis, to offset the decrease in coal.

The story continues to unfold despite the blip due to Sandy:

- COFC is up

- TOFC is down

- Overall ton miles are down

- Coal down

- Petroleum up dramatically.

Subscribe to:

Posts (Atom)