Last week could have been a "Seinfeld" week where it was the week about nothing. It was a very bad week (worst since June) for the stock market as people continue to anticipate poor earnings and forecasts for even slower earnings. It then had some nuggets of macroeconomic data which essentially said things were "flat".

I do want to start with the Producer Price Index. The

PPI went up by 1.1% ("Core" PPI held flat) v. an expected value of .7%. As can be seen in the graph below, this is a bounce back from the beginning of a decline. It is difficult to see how a recession could be in the near future when there is such inflation at the PPI (unless you think the increase is due to speculators hoarding commodities:

|

| FRED® PPI Index |

This will be an interesting trend to watch to see if we continue to have inflationary pressure at the PPI level which ultimately will need to come into the CPI or will be a drag on corporate earnings.

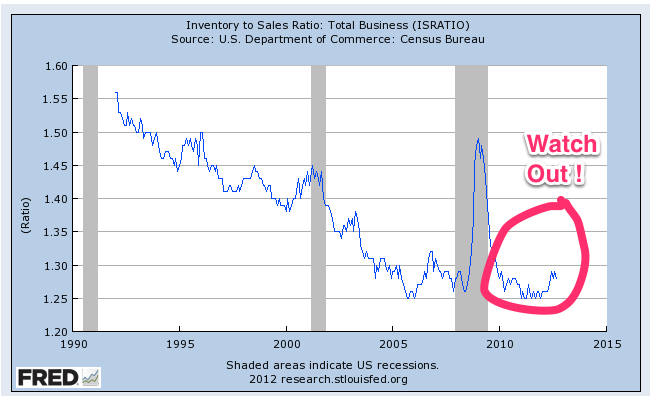

Inventory to Sales Ratio:

The vaulted inventory to sales ratio was released on Monday October 15 so I thought I would include it in this week's report. First, why is this number so important? What it shows is whether companies are

building inventory or are they

lowering inventory. If they are building inventory it is a signal that the economy is slowing since it usually takes a few months for companies to adjust to lower sales. There is seasonality to these numbers and for sure they are not adjusted for prices (if prices go up the

value of the inventory goes up but the quantity does not) but it is still a great indicator to watch.

|

| FRED® Inventory to Sales Ratio |

The graph shows this has increased over the last few months and it had started coming down but this month it actually increased ever so slightly. This is a clear indication the economy is "tilting" to slowing down and inventory is building. What do companies do when inventory starts building? They lay people off, slow down factories and slow down 2d and 3d tier purchases.

This is a key metric to follow and if you are not sure why just look at what happened during the recession - it ballooned.

Jobless Claims:

Initial jobless claims came in lower than expected (339K v. 370k expected) however I am going to let these numbers "mature" before I make any conclusions. There has been a lot of "noise" in these numbers lately so I am going to see some trends. By the way, I do not subscribe to the conspiracy theories related to these numbers but rather understand there are

real statistical reasons why the numbers are moving around. Let's see how it develops in the next few weeks.

Transportation Data:

In the last couple of weeks many indices have shown the transportation freight is slowing dramatically and rates have not only stabilized but in some cases are showing year over year declines. Transportation executives have "warned" already about slowing freight volumes and the inventory to sales ratio reported above would support the decrease in freight volumes in the future. All in all the story is not great for the near future for freight volumes. This report from Reuters a few weeks ago titled

Dow Transports Raise Warning Flag For US Economy says it best:

"Transportation and logistics companies are also worried. At least seven of them - FedEx, Norfolk Southern, UTi Worldwide (UTIW.O), Swift Transportation Co (SWFT.N), Arkansas Best Corp (ABFS.O), XPO Logistics Inc (XPO.N) and Werner Enterprises Inc (WERN.O) have scaled back their profit forecasts in recent weeks. United Parcel Service Inc (UPS.N) led the pack when it cut its outlook in July."

Morgan Stanley, Bank of America and others who follow the transportation industry clearly are indicating a slowing transportation spend and all the macroeconomic data would support that theory.

Advantage:

Clearly the data is showing a continued advantage for the shipper. This is another week of

Slight Advantage: Shipper®. Last week also reported this measurement so it is clear the extreme tightening of capacity and drivers and its effects on rates is being offset by the slowing economy and the potential for a slowing economy (yes, the negative feedback loop actually will effect this even more).