The Cass Freight Index report for July 2012 was somewhat anti-climatic for those of us who follow freight and knew we were in the depth of the great slowdown of 2012. The "phone bank" report (which measures the direction of phone calls from a fictional transportation manager's desk) reported far more incoming calls from carriers looking for freight than outbound calls searching for trucks and this has been true for at least two months now.

OK, I admit that is not a scientific index however if you are close to the business and have a grasp on that general topic it is a highly effective predictor of freight.

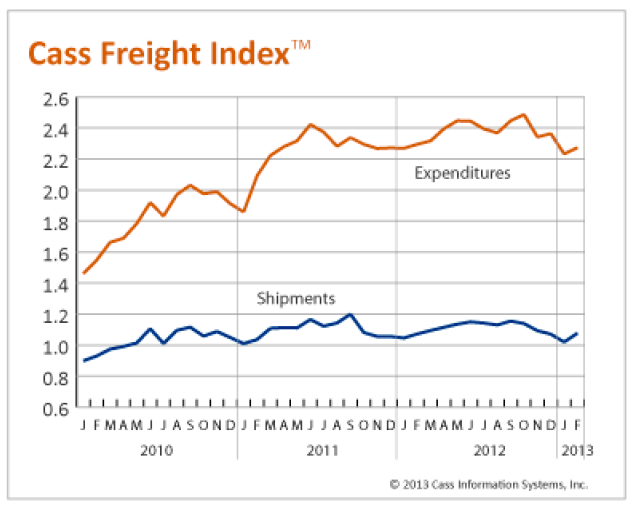

|

| Cass Freight Index - July 2012 |

We see from this index that essentially expenditures have leveled off really since June of 2011 with just a little bump at the beginning of Q2 in 2012. I attribute both years' early bumps as price / volume "hype" and not reality. Each of the last two years has begun with a "great hope" of where rates and the economy is going only to become disappointing by summer and a steadying of rates. A good and experienced transportation manager will see this trend and ensure they do not buy into the early year hype every year.

At the beginning of every year the transportation company sales people will show up with all sorts of data to tell you "this is the year" where we will hit a massive capacity crunch so you better "pay up now" to be taken care of later. A great story which makes for great industry journalism however the empirical evidence suggests it is, in fact, all hype and those who remain calm in the face of the story will be better off.

A key question though is how can all these companies (shippers) report great earnings, the market is very high ( Dow at 13,175.64 as of this writing) and yet the shipments and movement of goods is stagnant? I have a few theories (I freely admit these are theories however the data is showing this to be more and more true).

First, the economy is a more services and financial economy than it is a "things" economy. While we still consume the manufactured goods we generally do not make them. This means an entire portion of the former economy shipments is gone and that is inbound to manufacturing. The outbound is still there however the inbound is gone. The inbound freight is in China and Mexico and other low cost countries. Those who say they love being in trucking because their jobs cannot move overseas are wrong. The inbound jobs have moved overseas along with the inbound freight.

This of course follows the manufacturing base so if manufacturing truly does return to the United States (the jury is out on this) then the inbound will follow back.

Second, the great work on sustainability, minimizing packaging, routing efficiencies etc have all led to being able to move the same amount of goods with lesser number of vehicles. This movement is good for all of us in the world however it does decrease the raw demand for trucks. Just think of televisions. If the economy sells a million T.V.s this year (a made up number just to illustrate the point) they are all about 1" thick. 10 years ago if 1 million T.V's were sold they all were about 3 feet deep (packaged). That is a lot of trucks.

There is not only minimization of the product size but there is also the elimination of the physical product (think e-books. iTunes for CDs etc.).

So, my conclusion is you cannot compare the GDP numbers of today relative to prior year GDP numbers as if there is a straight correlation between the level of GDP and the amount of goods moving in terms of cube size (which is the driver of number of boxes needed). Clearly there is some kind of correlation but it is not as direct as it would have been 10 - 15 years ago. The economy can grow with less physical product moving.

Finally, the lesson learned of the last two years is clear: "Be Not Afraid"! at the beginning of the year. Don't buy the hype, be patient, watch the data and let the economy play out. You get

no credit (regardless of what the sales person tells you) for being an early mover on rate increases.