In an article today titled "At Ports, A Sign of Altered Supply Chains", they discuss the muted growth (or at least not shrink) of the trucking and ocean business. The cause? You guessed it - the fact that inventories are high, the consumer is moving to on line purchasing, and the more disciplined approach to inventory management. There are some key shifts happening:

- Demand Sensing Supply Chains: These have finally come into their own. Companies are much better at identifying the purchase trends and immediately shifting inventory purchases to adjust. If the consumer slows (or moves from apparel to electronics for example), Demand Sensing Supply Chains adjust almost in real time. Gone are the days of huge inventory buys "just in case".

- On Line Purchases and The Death of Excess Inventory: Anyone who has managed inventory knows these key tenets of inventory management: As you move inventory out and disperse it among stores or other storage points, your forecast accuracy decreases, your errors increase and the likelihood you will "orphan" inventory in the network increases dramatically.

To solve these gaps in information, you generally overbuy inventory to keep "in stocks" high.The inventory benefits of on line are clear: Far fewer inventory points (probably 4 at most) result in much higher accuracy which translates into far fewer inventory dollars to service the same consumer base. This, of course, translates into much less transportation needed. Those who say it does not matter, we are selling the same amount of stuff, do not know how the "laws of inventory" work. - The Growth of The Supply Chain Data Scientist: This is an entirely new field in supply chain and is different than just being an analyst. This is deep diving into data, pulling "fuzzy" data points together and identifying trends. These people see changes in buying patterns far earlier than ever before and provide that information to management which responds far faster than ever before. Inventory buys can be shut off in a nano second.

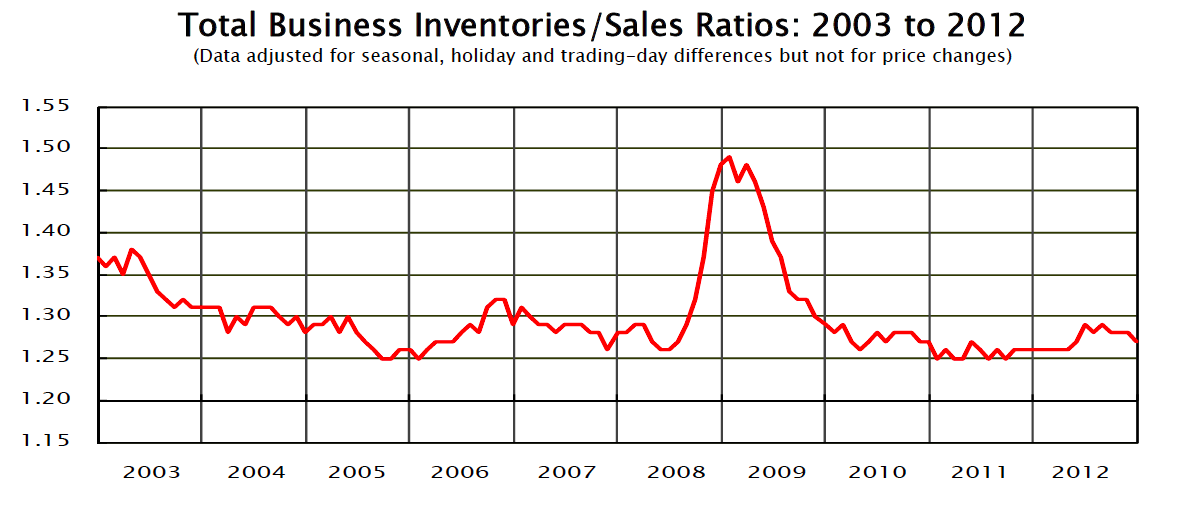

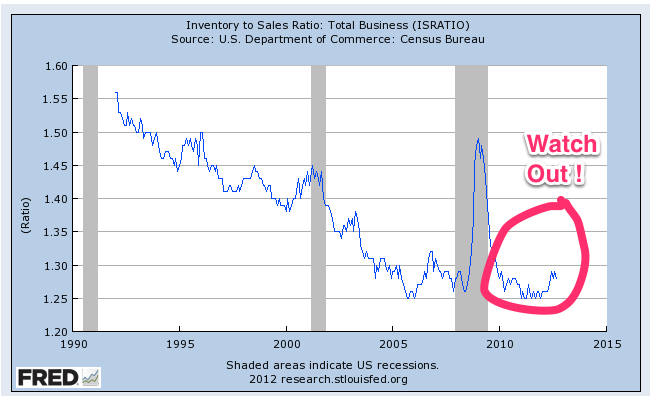

These factors are resulting in a far more disciplined inventory management process. We have been in an "over inventoried" position, in the aggregate, for a very long time and I have been predicting this will keep the demand for transportation services muted. This is what is happening.

Source: Wall Street Journal